Local Court Fee Increases Associated with Increased Jail Detention, New Research Finds

New research led by the Public Affairs Research Council of Alabama (PARCA) and MDRC indicates that each additional $100 in cumulative court fees for criminal cases is associated with an additional 34 jail detentions per 100,000 people at the county level. This small but significant increase suggests that fee increases could increase detention rather than deter it.

Counties often say local fee increases are needed to offset costs associated with processing criminal cases. Counties also pay the cost of housing people in their jails. This research suggests that new revenue from local fee increases should be weighed against the new costs (both social and fiscal) from housing more people in jail.

Beyond the Democratic and Republican primary elections scheduled for May 19, voters will decide the fate of two statewide amendments to the Alabama Constitution.

One would prevent local district attorneys’ salaries from being reduced during an elected term of office. Another would give judges discretion to deny bail to people charged with certain crimes.

Those amendments will be listed on the ballot in both the Republican and Democratic primaries. Alabama is an open primary state, which means voters don’t have to register with a party to participate in a primary. A voter simply requests the ballot of the primary they want to vote in.

If the voter doesn’t wish to vote in either party’s primary, he or she can request an amendment-only ballot.

PARCA has provided an objective, nonpartisan analysis of both amendments.

Drop in International Migration Slows Net Population Growth in Most of Alabama Counties

Decreasing immigration from abroad slowed population growth across Alabama’s counties in 2024 and 2025, though suburban counties and growth magnets in north and south Alabama continued to add new residents. The one-year metro population growth rate for Huntsville (3%) and Baldwin County (2%) put both among the fastest growing Metropolitan Statistical Areas (MSAs) in the US, with Huntsville at No. 6 and Baldwin County at No. 11.

Nationwide, the rate of population growth slowed sharply.

The new estimates released by the U.S. Census Bureau cover the period between July 1, 2024 and July 1, 2025. State-level estimates were released earlier this year. A PARCA analysis of that data showed that Alabama’s population growth hit a peak in 2024, driven in equal parts by international migration, new residents moving to Alabama from other countries, and domestic migration, people moving to Alabama from other U.S. states.

In 2025, the international component dropped sharply, while domestic migration edged down modestly. Deaths outnumbered births in Alabama at large and in all but 17 of Alabama’s 67 counties. Statewide and in most counties, the population would be decreasing without growth through domestic or international migration.

Figure 2. Comparing International Migration in Alabama 2024 vs. 2025

In 2024, central urban counties, like Jefferson, Montgomery, and Mobile, were receiving the bulk of new migrants from abroad. Population increases from international migration helped offset the population decline from people moving from those central counties to surrounding suburban counties or to other states.

However, with the drop in international immigration in 2025, Jefferson and Mobile counties lost population in the latest estimates. In Jefferson County, international migration decreased by almost 2,500 compared to 2024. Nearly 3,000 Jefferson County residents moved to other counties or states in 2025. After accounting for natural change and net migration, Jefferson County’s population decreased by 843 residents. Similar trends led to an estimated population decrease of 535 in Mobile. Montgomery County’s natural increase, plus a decline in outmigration, kept its population about even, increasing by 2, according to the estimates.

Figure 3. Population Change and Migration Components, 2025

National Perspective

These population dynamics within metro areas are not unique to Alabama. In its analysis of 2025 data, the Census Bureau noted that among large metro areas, the fastest-growing counties tended to be on the outer edges, indicating a continuing trend toward suburbanization. Meanwhile, central counties tend to draw the greatest number of international migrants.

For example, the central counties in the Nashville and Atlanta metros also see a net outflow of domestic residents. However, in both those cases, those central counties still attracted enough international immigrants to offset domestic outmigration. And those counties also lie at the center of some of the fastest-growing metropolitan areas in the country.

Figure 4. USA Map of Population Change By Metropolitan Statistical Area, 2025

The decline in inflows of international residents depressed growth in central counties and slowed metropolitan growth rates nationwide. The Census Bureau noted that growth in metro areas declined sharply. Average MSA growth was 1.1% between 2023 and 2024, but fell to 0.6% between 2024 and 2025.

Population growth is occurring disproportionately in southern coastal counties and in metro areas in the south. According to Census:

Geographically, many of the fastest-growing counties were in states along the Southeast coast of the United States, including Florida, Georgia, South Carolina, North Carolina, and Virginia.

Among counties with populations of 20,000 or more, nine of the top 10 fastest-growing counties were in the South, as were 45 out of the top 50.

Figure 5. USA Map by County of Rate of Change, 2025

Growth Spots

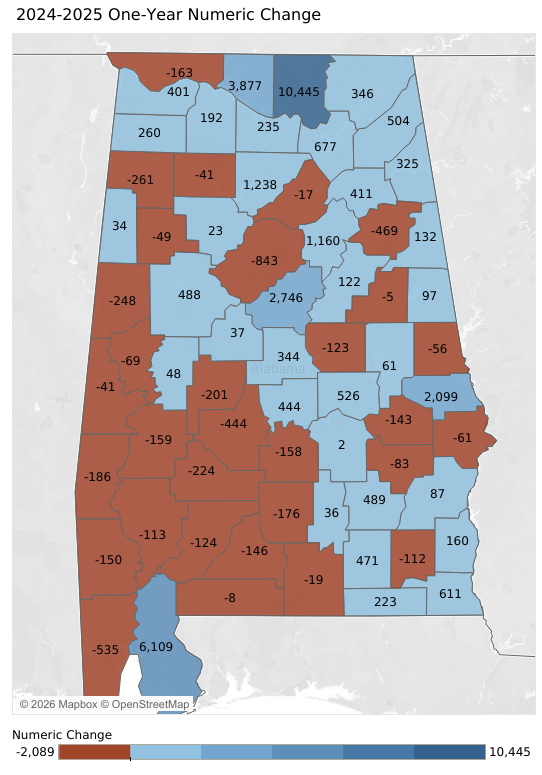

Madison County, home to Huntsville, continued to add more residents than any other county in Alabama. Growth from domestic migration increased in Madison County, which added more than 10,000 people, even as international immigration decreased.

Figure 6. Population Change and Migration Components, 2025

In neighboring Limestone County, growth tapered as international immigration decreased. However, in adding an estimated 3,285 residents, Limestone continued to rank among the nation’s fastest-growing counties with a 3.3% population increase in 2025. Together, Limestone and Madison County make up the Huntsville Metropolitan Statistical Area, which in 2025 was the nation’s 6th-fastest-growing MSA.

Figure 7. Percentage Population Change in Alabama MSAs

Alabama’s second-fastest-growing MSA consists of just Baldwin County and is officially known as the Daphne-Fairhope-Foley MSA. That MSA also continued to grow rapidly, as part of the growth pattern Census noted: people moving to southern counties along the Atlantic and Gulf coasts.

Despite Mobile County being right next door, Baldwin and Mobile are considered two separate MSAs. According to the Census Bureau’s analysis of commuting patterns, there is not enough daily interchange of populations between the two counties to consider them a single MSA. Mobile County’s population declined, in part due to a drop in international migration.

Figure 8. Numeric Change in Alabama MSAs

Alabama’s largest MSA is Birmingham, which now includes seven counties: Jefferson, Shelby, St. Clair, Blount, Walker, Chilton, and Bibb, with a population of 1.2 million people. That’s more than double the size of Huntsville, but Birmingham’s MSA is growing more slowly.

In 2025, the MSA added 3,450 people. Most of that growth occurred in Shelby County, which added 2,746 new residents, and St. Clair County, which added 1,160. That put both those counties in the Alabama top 10 for growth, both in pace of growth and number added. Walker, Bibb, and Chilton experienced modest gains. Together, that was enough to offset the decline in Jefferson and Blount counties.

The Auburn-Opelika MSA, which consists of Lee and Macon counties, grew by almost 2,000.

Dothan’s MSA, which includes Geneva, Houston, and Henry counties, added about 1,000 in total. Tuscaloosa County added almost 500 new residents, and Hale County added about 50, but the other two counties in the Tuscaloosa MSA, Greene and Pickens, lost population. So, in total, the four-county MSA was up by just over 300 residents.

Over in East Alabama, Etowah County, which makes up the Gadsden MSA, has posted positive growth for the past three years after several years of decline, adding 411 in 2025. Calhoun County, the Anniston-Oxford MSA grew in 2022 and 2023, but in 2024 and 2025, the estimates point to population decline, a decrease of 469 in 2025.

Huntsville MSA’s north Alabama neighbors in the Decatur and Florence-Muscle Shoals MSA’s grew modestly. In Decatur, Morgan, and Lawrence counties, each added about 200 new residents, a fourth straight year of growth. The Shoals, made up of Colbert and Lauderdale counties, have both been gathering steam in population growth during the current decade, though Lauderdale was estimated to have had a decline of 163 residents in 2025.

Overall, 36 Alabama counties gained population, but only 7 added more than 1,000 people; 31 counties saw population declines.

Rates of Change

The counties losing the population the fastest are in Alabama’s Black Belt. And that trend continued in 2025. Perry, Lowndes, Willcox, Dallas, and Greene counties have each lost 8% or more of their population since 2020. There are now five counties with fewer than 10,000 residents: Bullock, Wilcox, Lowndes, Perry, and Greene.

Figure 9. Rate of Change, Domestic Migration, 2025

Multiple factors are conspiring to drain population from rural Alabama counties. Rural counties also tend not to attract new immigrants from other counties. Domestic migration is also typically low to negative, with younger residents often moving to metropolitan counties where jobs are concentrated. As younger people move away in search of opportunity, the population becomes disproportionately old.

As the Baby Boom ages, that large cohort is beginning to experience increased mortality. As the average age increases, the death rate increases. And since younger people have tended to move to metros, the birth rate has declined.

Figure 10. Rate of Change, Death, 2025

The pattern isn’t confined to rural Alabama. It is also pronounced in the former coal country in the Appalachians, in the Mississippi Delta, and in portions of the West and Midwest.

Figure 11. USA Rate of Population Change by County

Keys to Success in College and Career Readiness

This spring, all Alabama high school graduates will have to earn a marker of college and/or career readiness in order to graduate.1

In this installment of PARCA’s Keys to Success series, we visit Opp High School, which has been one of the state’s most successful schools at producing college and career-ready graduates. In fact, for five years running, more seniors were college or career-ready (CCR) than actually earned a diploma.

In 2024, 94% of Opp’s seniors graduated (beating the state average of 92%), and 99% of seniors ended the year with a marker of college and career readiness, a CCR rate that is 10 percentage points higher than the state average.

How do they do it?

More attention per student thanks to small school size

A close dual enrollment partnership with the local community college

Creative use of practical, local opportunities for students to earn Career Technical Education credits and credentials

Practice and deliberate effort on the measures that qualify students for college readiness

PARCA’s Keys to Success series identifies schools and systems that are exceeding expectations and explores how they are doing it. The series aims to identify and share best practices.

Small Town Personalized Attention

The City of Opp, located in rural Covington County, was formerly a textile mill town. Despite the closing of the textile mills, Opp has maintained a stable population of around 6,700 people since 2000.

The school system produces between 80 and 90 graduates per year, which ranks among the 20 smallest school systems in the state. Opp’s percentage of students from economically disadvantaged households is higher than the state average. Thanks to federal anti-poverty education dollars, Opp’s per-student expenditure was slightly above the state average in 2023.

In some ways, that small size helps Opp. The high school is the center of activity and energy for the entire community. That keeps students and the community engaged.

“What is going on at school is the hottest thing in town. That is very much an asset for us,” said Opp High School Principal Matt Blake.

A smaller school can, in some instances, mean each student receives extra attention. For example, in addition to a traditional guidance counselor, Opp High School has a full-time career coach, who works with the counselor, to make sure all students have a plan to progress through school on a trajectory that points toward one of the “three e’s”: graduating from high school, either Enrolled, Employed, or Enlisted.

Student preparation for college and career readiness begins in middle school, with the career coach visiting students and making them aware of potential career pathways. During orientation, rising ninth graders and their parents are presented with career options, and students begin developing four-year plans to meet both academic and college- and career-readiness markers they’ll need to graduate.

Once at the high school, the counseling suite is highly visible, located at the top of the high school stairs, with glass windows for walls. The visibility serves as a reminder to students of the stream of opportunities available. Opp has a regular stream of visits from college, employment, and military recruiters.

When Blake moved to Opp from Gulf Shores in 2022, he brought his career coach, Courtney Blake, with him. She also happens to be his wife. The two have creatively conspired to leverage resources to expose students to college and career opportunities.

Community College Collaboration

A primary partner in the CCR enterprise is Opp’s community college, the MacArthur branch of Lurleen B Wallace Community College (LBW).

In the past, more than half of Opp graduates flowed into LBW after graduation. More recently, the relationship is even tighter and starts earlier through dual enrollment. Opp students, while still in high school, make up a healthy share of the college’s enrollment.

In fact, Opp now delivers all its college-caliber courses in partnership with LBW, rather than offering Advanced Placement courses at the high school.

In the 2024-2025 school year, Opp students took almost 400 credit hours at LBW, including college-level courses in English and history, calculus, biology, and psychology. That total also included about 52 career tech classes, including industrial maintenance, engines, computer science, and cosmetology. Opp High School students also took aviation courses through Enterprise State Community College.

Some students attend classes on the LBW campus. In other cases, an LBW instructor may come to the high school campus to lead class two days a week, with students led by Opp teachers the other three days, who focus on ACT prep skills and strategies. Opp High School also has its own teachers who are certified to teach dual-enrollment classes on campus at OHS, but through LBW.

Both academic and career-tech courses taken through LBW count toward degrees or certifications. The academic courses can be transferred to universities, allowing Opp graduates to start college with a bank of credits toward a degree.

Taking Creative Advantage of Available Opportunities

Opp isn’t a big city full of employers and businesses that can offer internships or sponsor training programs for high school students. But the Opp High has a tradition of Career and Technical Education programs that creatively intersect with school and community needs.

Plant Science teacher, Josh Kyser, is a graduate of the turfgrass management program he now leads. After graduating from Opp, he continued in the field at Auburn, which led to a career in golf course management and design.

Family ties eventually drew him back to Opp, and after a few twists and turns, he was recruited to serve as the City of Opp’s director of Parks and Recreation. The City maintains the high school’s fields, so he had a close relationship with the school. Eventually, high school leaders persuaded him to lead the program that had launched his career.

The horticulture class helps care for the school’s athletic fields, which, over time, can lead to students earning turfgrass management and plant biotechnology certifications. Meanwhile, through a competitive grant program, Opp won extra career-tech funding to put students to work and in class during the summer on a school field project.

The students worked with the City and the county on a project to grade and pave a road from the school to the athletic field. Through their summer work, the students earned money and certifications for operating skid steers, mini-excavators, and bulldozers. Those certifications have real value in the employment marketplace.

In another summer project, students in the plant biotechnology classes designed and constructed a pollinator garden. Students also planted and tended vegetable and herb gardens, projects that were also funded in part with CTE money won through a competitive grant.

This fall, that pollinator garden was fluttering with butterflies and darting with hummingbirds. The vegetable and herb gardens yielded beans, collards, Brussels sprouts, and other ingredients that contributed to a community banquet organized by the students in the food and nutrition program.

In preparing for the event, students earned ServeSafe certifications, a credential often required for those working in the restaurant industry. The preparation and execution also dovetailed with nutrition science course credits.

Increasing College Readiness

Opp High School has also ramped up student preparation for four-year colleges, focusing on improving performance on the ACT college admissions test.

Historically, most college-bound Opp graduates started at a community college, then transferred to four-year universities after earning college credits.

With the sharp rise in students taking community college courses in high school, students are in a better position to go straight to a four-year college after graduation. However, that means ACT scores take on more importance for college admission and scholarships.

Blake, who spent time as a football coach, recognizes the value of practice.

So, in his effort to improve student performance on the ACT, Blake created more opportunities for students to take the test. The school pays for ninth-graders to take the Pre-ACT, in addition to administering it to 10th-graders in the fall.

The school then offers students a first attempt at the ACT in the spring semester of their 10th-grade year.

In January, teachers begin reviewing the test and have students take a mock version of the ACT.

They take mock versions again in February. Using a digital test reader, students receive immediate results. Teachers identify questions that tripped up students and talk through the answers, and address the underlying skill.

Students participate in a two-day ACT boot camp. The school brings in an ACT specialist in Math and ELA to lead a two-day intensive review before the last mock exam. This allows students to use the strategies and tips from the last mock exam to build confidence in their abilities.

In late March, juniors take the real test, the required junior year administration.

Blake concedes that he has greatly increased the emphasis on the ACT. However, he doesn’t think that emphasis distracts from educational goals. “Test-taking skills aren’t frivolous,” he said. “It teaches problem-solving and critical thinking. And they’ll have to take similar tests in college or if they apply to graduate school.”

Results

Between 2023 and 2024, the percentage of students earning a benchmark score on the ACT leapt from 34% in 2023 to 52% in 2024, exceeding the state benchmarking rate of 42%

The Opp graduating class of 2024 posted major gains on the ACT in every subject, outperforming the state in all four subjects.

The college-going rate in Opp rose from 62% in 2022 to 68% in 2024, far exceeding the state college-going rate of 57%.

The gains were particularly pronounced in the percentage of students who went straight to a four-year college after graduating from high school, rising from 10% in 2022 to 31% in 2024.

Conclusion

Blake said Opp’s success has resulted from long-term planning by the school, students, the system, and the state.

The school works with students and parents, beginning in middle school, to chart a student’s path through choices and courses that lead to a college or career goal. The school works with local partners such as LBW Community College, Opp’s Mizell Memorial Hospital, and the City of Opp to expand work and internship opportunities for students.

The school also works with the system and the state to pay for enhanced opportunities. The school has been aggressive and creative in pursuing grants and establishing budget priorities in order to pay for novel CTE programs, summer work opportunities, and intensive ACT training for faculty and students.

As the requirement that all students earn a CCR credential goes into effect this fall, the State Department of Education and the governor’s office have indicated continued support for enhanced investment in College and Career Readiness. The Governor’s proposed budget maintains support for career coaches and for K-12 career tech programs and initiatives. The budget proposes increasing support for dual enrollment through the Alabama Community College System by $10 million. The Legislature will consider the budget during its session, which opened earlier this month.

Footnotes

In order to demonstrate college and career readiness, a student must achieve one of the following: 1. Score college-ready in at least one subject on the ACT 2. Score at the silver level or above on the WorkKeys Assessment. 3. Earn a passing score on an Advanced Placement or International Baccalaureate Exam. 4. Successfully earn a Career Technical Education credential or earn Career and Technical Education (CTE) completer status. 5. Earn dual enrollment credit at a college or university. 6. Successfully enlist in the military. 7. Complete a CTE program of study. 8. Complete an in-school youth apprenticeship. ↩︎

PARCA Partners with VOICES on the 2025 Alabama Kids Count Data Book

Since 1994, the Alabama Kids Count Data Book has documented and tracked the health, education, safety, and economic security of children at the state and county levels.

The Data Book serves as both a benchmark and roadmap for how children are faring and is used to raise visibility of children’s issues, identify areas of need, set priorities in child well-being and inform decision-making at the state and local levels.

The 2025 edition represents the 32nd installment of the organization’s long-running assessment of child well-being in Alabama. Unlike previous years, the Data Book will no longer be limited to a single annual release. Instead, VOICES plans to publish ongoing updates, analyses, and issue briefs throughout 2026.

“For more than three decades, the Data Book has helped Alabama understand how our children are doing,” said Dr. Tracye Strichik, executive director of VOICES for Alabama’s Children. “But children’s lives—and their mental health needs—are changing quickly. A digital, year-round approach allows us to respond with data that is timely, relevant, and actionable.”

See how children in all 67 counties of our state are faring in education, health, economic security, and more. VOICES believers that every child in Alabama should have access and opportunity to thrive and become all they can be, and hopes that by utilizing this book’s insights, we can identify the challenges, set priorities, track our progress, and achieve real outcomes for children and families.

The 2025 County Data Profiles are also available for each of Alabama’s 67 counties and the state. These four-page reports provide even more disaggregated data on the indicators presented in the 2025 Alabama Kids Count Data Book.

Want to see this data at the national level? Visit the national KIDS COUNT Data Center to access hundreds of indicators, download data and create reports and graphics!

How Alabama Taxes Compare, 2025

Each year, PARCA uses data from the U.S. Census Bureau’s Annual Survey of State and Local Finances to compare Alabama’s tax collections to all 50 states. The most recent data comes from the 2023 Fiscal Year.

In FY 2023, adjusted for population, Alabama collected less in state and local taxes than all but two other states, Tennessee and Mississippi, both of which cut taxes significantly in recent years.

Alabama’s per capita property tax collections are the lowest in the nation. That can help owners of homes, farms, and timberland but comes at the cost of a revenue deficit, leaving state and local governments with less to spend providing government services like education, health, and public safety.

Alabama’s state and local sales tax rates are among the highest in the U.S., compensating for low property taxes.

Alabama’s income tax, while technically graduated, does not provide the balancing effect on the regressivity of the entire tax system that graduated income taxes in other states do. Low-income workers begin paying taxes at a lower threshold than in any other state, and brackets top out at a low threshold as well. At the other end of the spectrum, Alabama is the only state that allows a full deduction for federal income taxes paid, a tax break that benefits high-income earners.

Alabama is home to 5,996 active 501(c)(3) organizations that file regular tax returns and report at least $25,000 in annual revenue or assets. Although more than 25,000 nonprofits are registered in the state, many are inactive. The active group represents the real working infrastructure of civic life—from child abuse prevention and mental health services to workforce training, arts, and conservation.

Relative size

Alabama has 114.6 nonprofits per 100,000 people—ranking 40th nationally. Its density is lower than most states, suggesting opportunity for measured growth rather than oversaturation.

Economic footprint

Active nonprofits generate $16.9 billion in annual revenue, but that total is highly concentrated: 0.35% of organizations (the 21 largest) account for nearly half of all income. The median nonprofit operates on about $200,000 a year, with two-thirds reporting less than $500,000.

Public investment

Between 2015 and 2025, Alabama nonprofits received $5.5 billion in federal awards—an average of $553 million per year. More than 60% of those dollars flow through the U.S. Department of Health and Human Services; most reach communities through state agencies such as the Alabama Department of Economic and Community Affairs (ADECA), the Alabama Department of Public Health (ADPH), and the Department of Early Childhood Education.

Philanthropic capacity

Alabama’s 822 foundations hold $4.5 billion in assets—ranking 49th per capita. Assuming a typical 5.6% payout, foundations could distribute about $226 million per year, only one-third of recent federal funding. Private philanthropy cannot replace sustained public investment.

Key finding

Alabama’s progress depends on collaboration among government, philanthropy, and community organizations. Nonprofits are not a substitute for government; they are its local expression. Strengthening this partnership—through data transparency, diversified funding, and civic trust—is essential to building a resilient Alabama.

Lower Fines and Fees Raise MORE Revenue than Higher Fines and Fees, Study Finds

New research indicates that lower fines and fees raise more revenue than higher ones, and that a “collections fee” that is supposed to incentivize payment is instead associated with greater debt.

The report, Findings from the Jefferson County Equitable Fines and Fees Project from MDRC, provides insight into an issue the Legislature is struggling to address: Alabama’s patchwork system of fees and court costs. Earlier this year, the Legislature established a Joint Interim Study Commission on Court Costs to examine ways to reform and standardize the court cost system. The Commission will report to the Legislature in its upcoming session early next year.

The new report, a Jefferson County case study, uses five years of case-level data to examine drivers of court debt accumulation over time. PARCA Senior Research Associate Leah Nelson was co-founder and co-principal investigator on the project.

What are fines and fees?

Every year, criminal courts in Alabama assess an unknown amount in fines, fees, court costs, and restitution. Fines are intended as punishment, while fees (including court costs) are meant to cover the expenses associated with the case. Some people are also assessed restitution if the offense they were convicted of resulted in a financial loss to a victim.

Although the total amounts assessed and outstanding across Alabama’s criminal courts are unknown, annual collections are substantial. Criminal courts drew a total of nearly $114 million in 2024 alone, including $6.1 million that remained within the court system, while $80 million was disbursed to non-court entities such as the General Fund, the Alabama Department of Economic and Community Affairs, the State Department of Education, and American Village at Montevallo. And, finally, $12.7 million in restitution was distributed to victims.

Fines are supposed to deter involvement in the criminal justice system, while fees exist to recoup the cost of court involvement, while also generating revenue for the state. New research suggests that higher fines and fees are counterproductive: producing less revenue, creating higher levels of unpaid debt, and prolonging individuals’ involvement with the criminal justice system.

People assessed lower amounts at the time of sentencing paid more money and were more likely to pay their debt down to zero, as compared to people assessed higher amounts (who typically saw their balances increase over time). In other words, people who were assessed less debt were not only more likely to finish paying, but they paid more money.

A 30% collection fee assessed when people are 90 days late with their payments resulted in higher unpaid balances and a decreased likelihood of paying off their fines and fees.

Indigent people were assessed higher financial penalties than their more affluent peers.

Victims may never receive, or fully receive, financial restitution because of how fines and fees revenue is distributed.

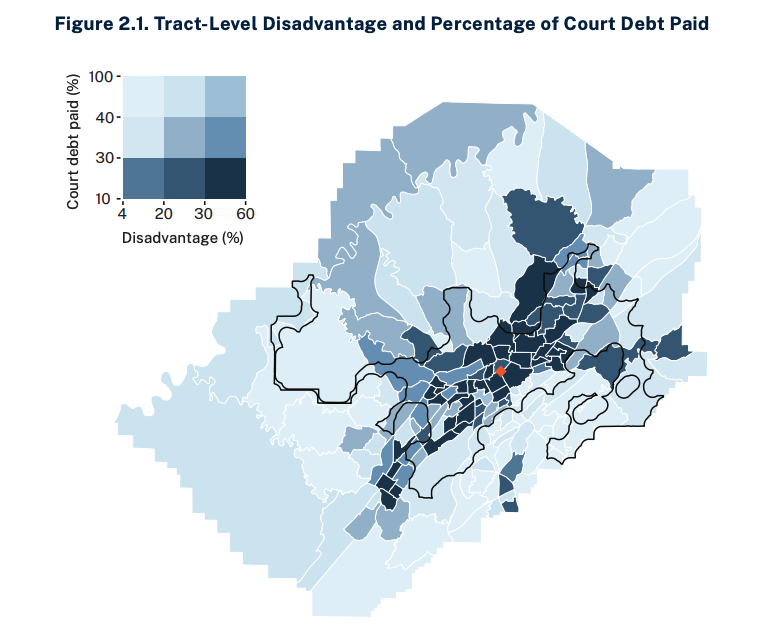

Court debt was concentrated in census tracts marked by high levels of concentrated disadvantage, a composite metric that measures a given location’s level of socioeconomic challenges.

How does the system work?

Assessment of debt

Fines, fees, and costs are assessed at the time of sentencing in nearly all criminal cases where a person is found guilty. Amounts are set by statute. A typical sentence simply includes a note that the defendant is to pay fines, fees, and costs, along with any restitution that may be due. Judges do not typically say the amount out loud at the time sentencing, so it is common for people to agree to pay as part of a plea without knowing exactly how much they will owe. While judges are required to assess fines and fees, under the Alabama Rules of Criminal Procedure (Rule 26.11), they have broad discretion to set payment plans or even forgive debt if a person is unable to pay. The same rule allows judges to incarcerate people who willfully refuse to pay.

Fines and fees may be the only sanction a person faces in a low-level case. In more serious cases, fines and fees are imposed in addition to supervision or incarceration. Many people who are assessed fines and fees are unable to pay them all at once, and it is common for judges to allow them to pay in installments.

Research shows that Alabama residents who owe fines and fees over long periods of time often make desperate choices as they seek to stay current on their debt. A 2018 survey showed that 83% gave up a basic need like rent, car payments, or medication; 44% took out a payday loan; and 38% percent admitted to engaging in unlawful activity – usually selling drugs, stealing, or sex work – in order to keep up with their court payments.

Even so, half of those surveyed told researchers they had been jailed in connection with unpaid debt. “Every time I turn around, they got a warrant out because I can’t pay,” one man said. “Having to fear the police is not right because of debt.”

Distribution of revenue

Alabama Code sections related to fees name the entity or entities to which revenue collected from fees must be disbursed. However, the order in which money is disbursed falls to the discretion of the Chief Justice of the Alabama Supreme Court. Over the decades, default priorities have been programmed into the State Judicial Information System (SJIS), which is the software used by district and circuit courts to docket and track cases.

Disbursements operate on a “cascade” basis, meaning the top priority entity must be paid in full before the next entity in line gets a single dollar. Under the current default priority system, court costs are paid first, and victims who are owed restitution are paid last. If a person who owes fines and fees falls behind on their payments by more than 90 days, they are automatically assessed a “collections fee” of 30% of what they owe. If assessed, the collections fee becomes the top priority and must be satisfied in full before any other fund receives a share of revenue. Judges have the authority to re-order priorities (for instance, to put restitution at the top of the list), but must issue reprioritization orders on a case-by-case basis.

Findings from the Jefferson County Equitable Fines and Fees (JEFF) Project

Following the money

The average initial amount assessed in cases included in the JEFF sample was $1,253.52.

42% of people pay nothing at all toward their fines and fees.

People were more likely to pay who were:

Not indigent

50% of non-indigent people paid off their full debt, compared to 16% of people who were represented by public defenders due to low income)

Facing lower fines

People in the lowest quartile of court debt assessed (a median debt of $121) tended to pay off their debt. By contrast, people in the top quartile (with a median initial assessment of $1,827) saw their debt nearly double over the five-year period studied.

Over 60% of cases in the sample were assessed a 30% collections fee, which is added to the balance when a person fails to pay anything toward their balance for 90 days.

Collections fees were associated with an average $827 increase in unpaid balances, with only $262 in payments on average after the fee was imposed. Those assessed the fee were less likely to pay off their debt.

In other words, the collection fee, which is intended to increase revenue, is more associated with increased debt.

Geographic Concentration

Geographically, debt was concentrated in the central valley area of Jefferson County, which is also home to a disproportionate percentage of Jefferson County’s Black residents.

People who lived in census tracts marked by concentrated disadvantage were much less likely to pay down their debt as compared with people in more affluent areas of the county. A one-percentage-point increase in concentrated disadvantage corresponds with 13% less court debt paid.

The human consequences of fines and fees

Most people (71%) in the sample were defended by a public defender, meaning that a judge determined they were indigent at the time of trial. Unsurprisingly, people who were indigent paid less toward their court debt than those who could afford to hire a lawyer. More surprisingly, JEFF researchers found that across all charges, indigent people were assessed higher financial penalties than their more affluent peers.

In interviews, court practitioners expressed frustration with the system. They described administrative headaches associated with attempting to keep up with debtors who often have unstable housing situations and don’t receive notices reminding them to pay. They felt that the 30% collections fee was deeply problematic, but worried that the district attorney’s office couldn’t operate without the revenue it generates. They expressed a broad desire to see court and law enforcement operations fully funded by the legislative branch, rather than being tasked with generating their own revenue.

Meanwhile, people who owed court debt described feelings of fear. Few were aware that they were allowed to ask for their court debt to be forgiven, and many thought the money was kept by local police or courts. (In fact, most of it flows back to the state.) Discussing the dread associated with owing court debt, one person said, “It’s like drawing an X on your back and I got you forever.”

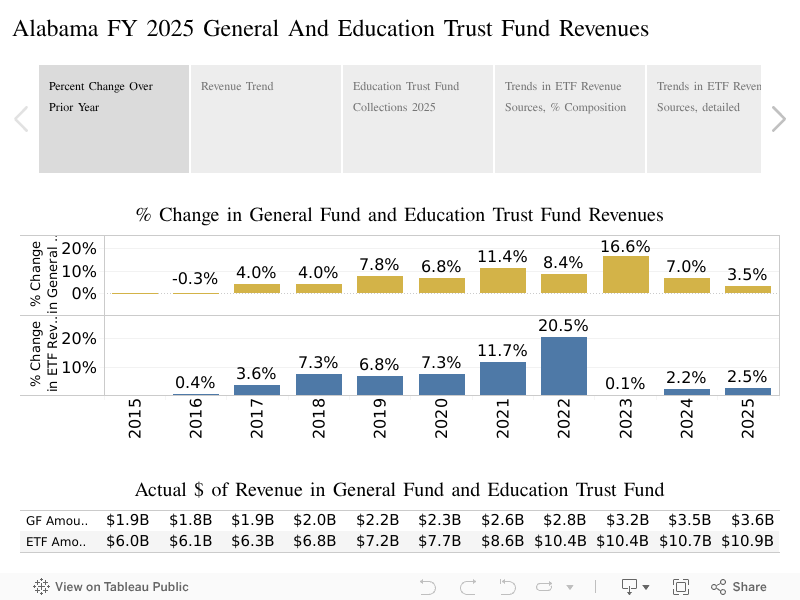

State Tax Revenues Cool in FY 2025

Tax revenues flowing into Alabama state government returned to a more normal rate of growth in 2025, after several years of unusually high gains. Revenue flowing into both the General Fund and the Education Trust Fund grew at about the rate of inflation.

A combination of unusual conditions, including historically low unemployment and an unprecedented level of Covid-relief and economic stimulus sent to the state by the federal government, produced large surges in collections. Inflation, wage growth, and high interest rates on state deposits have continued to keep revenue growth elevated, but are expected to continue to taper in FY 2026.

Click the link above for the full report, or view below.

New Data Shows Progress on Third Grade Reading Continues

Due to a new higher standard, the number and percentage of third graders who failed to meet the grade-level reading benchmark rose in 2025. However, taking the higher standard into account, this year’s third graders showed continued improvement, indicating that the state’s focus on improving early grades literacy is continuing to pay dividends.

This spring, 11.6% of students failed to reach the benchmark on the Reading portion of the state’s standardized test, the Alabama Comprehensive Assessment Program (ACAP). Had the higher bar been in place in 2024, 13.7% of 3rd graders would have scored below the cut. In 2023, 20.8% of 3rd Graders would have scored below the cut.

In 2025, more students, 49,460, cleared the bar despite the higher standard. At the same time, more students, 6,470, fell below the reading sufficiency benchmark. The 2025 cohort of third graders is larger than previous years. That could mean more students will be required to repeat third grade. However, students who scored below the benchmark are offered intensive summer instruction, retesting, and alternative ways to qualify for promotion.

Improved performance

For the second year, the biggest gains in the percentage of third graders clearing the reading benchmark have occurred predominantly in rural school systems in the Black Belt. Those systems have high rates of economic disadvantage among students and have traditionally trailed other systems on various academic measures, but they have been making gains in reading.

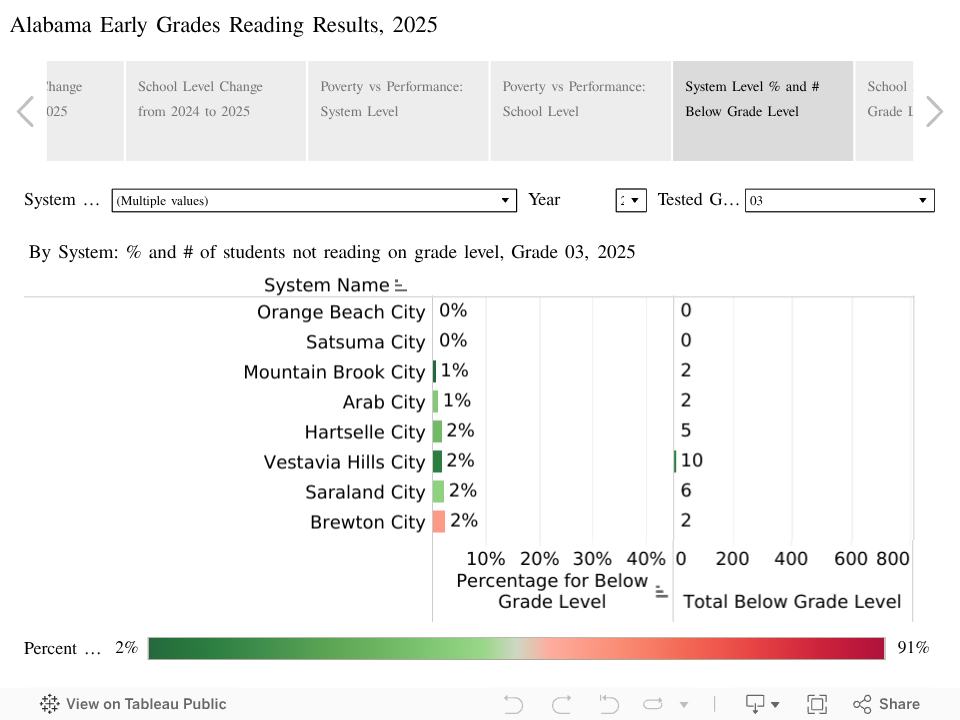

This year, only 4% of Wilcox County students scored below grade level. That puts the system in the top 20 for performance, even though 91% of students in Wilcox County are economically disadvantaged.

Two systems, Orange Beach and Satsuma, had all their tested third graders reading on grade.

Breaking the Connection Between Poverty and Poor Reading Performance

While there is still a correlation between higher levels of economic disadvantage and high rates of reading struggles, the relationship has gotten weaker over time, with more high-poverty systems, particularly in rural areas, improving performance.

Other high-poverty systems, often in urban areas, are still struggling to close the gap. Large urban systems like Montgomery County and Birmingham City have higher concentrations and larger numbers of students testing below grade level. However, those systems also have magnet schools where all students achieved the reading benchmark. Within larger school systems, schools with similar demographics vary significantly when it comes to reading results.

The scatterplot chart below compares the percentage of students in the school who are below grade level on reading to the percentage of students from economically disadvantaged households. The higher on the chart a system is, the better its reading performance. The systems shaded green and lying to the right are schools with lower economic disadvantage. The size of the system’s circle corresponds to the number of third graders who failed to achieve the reading benchmark.

Schools

Despite the higher bar, in 42 schools, all third graders who were tested passed the reading benchmark. That included Princeton Elementary in the Birmingham system and three schools in the Montgomery County System: Bear Exploration Center, Macmillan International at McKee, and Forest Avenue Elementary School. The schools where all third graders met the benchmark ranged from Georgiana, where 86% of students are from economically disadvantaged households, to Mountain Brook and Crestline elementary schools, where only 2% of students are economically disadvantaged.

The two schools with the largest number of third graders who are below grade level in reading are virtual schools: the Alabama Virtual Academy at Eufaula City Schools, where 421 students, or 37%, failed to make the benchmark, and the Alabama Connections Academy of Limestone County, where 290 students, or 32% scored under the benchmark.

For Students Who Failed to Score At or Above the Benchmark

The 6,480 students who failed to reach the benchmark are in jeopardy of being required to repeat 3rd grade, under the terms of the Alabama Literacy Act. However, there are several routes for promotion to the fourth grade.

Students who failed to clear the new reading sufficiency benchmark have access to intensive summer literacy camps sponsored by local school systems. After the intervention, they will be able to retest.

If they still fail to clear the bar, teachers and school officials have alternative means for evaluating the students’ reading skills. Other good-faith exemptions exist. In 2024, 4,808 students failed to pass the reading sufficiency benchmark. After retesting and applying exemptions, only 452 students were retained due to the Literacy Act, according to the Alabama Daily News reporting.

Second Grade Results

Also included in the data release were second-grade results. The cut score also went up for second grade. The second-grade score is intentionally set at a higher threshold so that more students who might be encountering reading struggles can be identified and receive intervention. Due to the higher bar, more students failed to meet the grade level sufficiency benchmark, 19% in 2025 compared to 17% in 2024. The 10,423 second-grade students who scored below the benchmark were encouraged to attend summer literacy camps and should receive special attention throughout their third-grade year.

Background

The intense interest in 3rd-grade reading is the result of the 2019 Literacy Act. The Act was modeled on similar legislation enacted in Florida and Mississippi. Both of those states saw large gains in reading performance on national standardized tests. The laws are based on the premise that students have to be reading on grade level by fourth grade. Students are taught to read from Kindergarten through third grade. In fourth grade, students are expected to read material to learn.

Numerous studies have found that students who aren’t reading on grade level by fourth grade are more likely to struggle academically and fail to complete high school. Low literacy skills are associated with difficulties in the job market and poor health outcomes.

While the Literacy Act’s grade retention provision received attention, the more consequential portions of the bill were its increased investment in improving literacy instruction, early screening for reading difficulties, and requirements for interventions and communication with parents. The Act re-energized the Alabama Reading Initiative and led to statewide training of teachers in techniques grounded in the science of reading.

Since implementation, Alabama has seen various measures of reading performance rise. Alabama is one of only two states (Louisiana is the other) in which 4th-grade students are performing better in reading than before the COVID-19 pandemic, according to the 2024 National Assessment of Education Progress (NAEP).