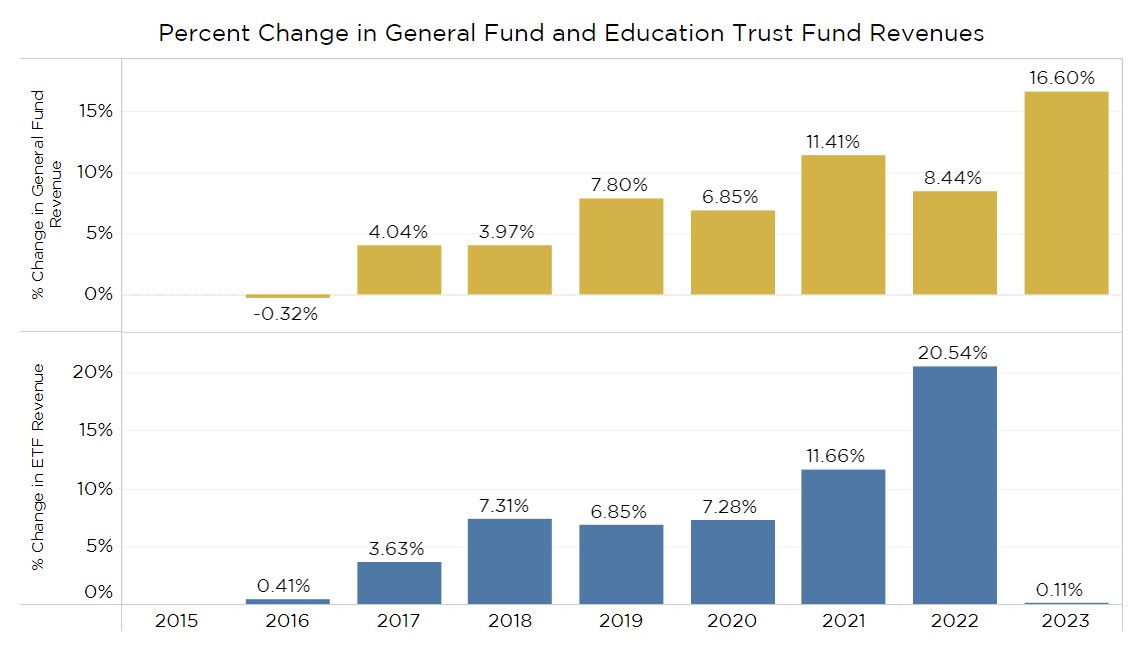

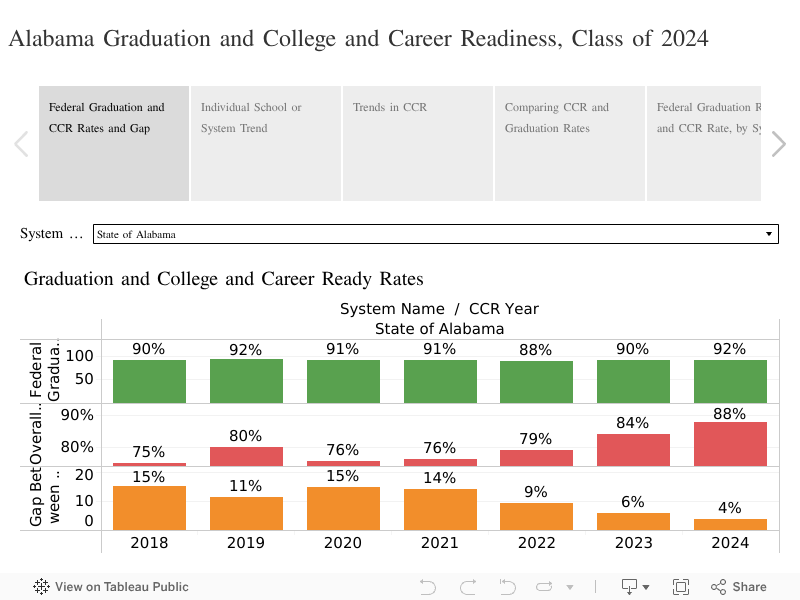

Alabama’s public high school graduation rate tied its all-time high in 2024, while the Class of 2024 also set a new record for the percentage of graduates designated ready for college and career, according to new data released by the Alabama Department of Education.

Among 2024’s senior class, 88% had earned a college and career-ready (CCR) designation, a jump of 4 percentage points over the rate for the Class of 2023. That progress also narrows the gap between the graduation and CCR rates to 4 percentage points, the smallest gap ever.

Alabama’s high school graduation rate has been rising since 2012, when the state set a goal that 90% of ninth graders would persist and graduate four years later. As the state’s public schools made progress toward and ultimately achieved that goal, policymakers focused on the gap between the graduation and CCR rates. Though more students were graduating, many weren’t leaving with the credentials to prove they were ready to enter college or the workforce.

In 2023, the Alabama Legislature passed a law requiring that by Spring of 2026, all graduates will have to have earned a CCR designation in order to receive a diploma. Schools have been moving toward that goal. In 2024, over 50 high schools reported a 100% graduation rate, and more than 40 reported a 100% college and career readiness rate.

Multiple Ways to Demonstrate College and Career Readiness

The Class of 2024 produced a jump in the on-time graduation rate and in multiple categories of college and career readiness.

School systems and high schools have different approaches to providing students with pathways to the CCR designation. Academic magnet schools and affluent suburban systems have higher percentages of students scoring college-ready on the ACT or by earning a qualifying score (3 or above) on an Advanced Placement test. Advanced Placement (AP) courses are college-level courses taught by high school faculty. International Baccalaureate (IB) courses are similar and also count toward CCR. Other schools, usually cooperating with the local community college, may give most students access to college courses. Many schools encourage enrollment in career technical education courses and reach over 90 percent of students through such offerings. Successful entry into the military and completing an approved youth apprenticeship is also an option.

Career Technical Education

More students are participating in career technical education courses, high school courses linked to career skills and training. The number and percentage of students demonstrating college and career readiness through completing a course in career technical education and earning an industry-recognized credential rose to 24,535, up from 21,640 in 2023. In the class of 2024, 47% of students earned a credential that should be recognized as valuable to a prospective employer, a 6-percentage point increase.

Dual Enrollment

The number and percentage of students earning college credit, mostly through dual enrollment at a community college, also rose substantially from 21% of students in 2023 to 26% for the Class of 2024. Statewide, 13,891 students had earned credit through successfully completing a college course during high school, an increase of over 2,500 from the Class of 2023.

ACT

The percentage of Alabama public high school graduates earning a benchmark score on the ACT rose to 42%, up from 40% in 2023. ACT, the standardized test that predicts student readiness for college-level coursework, is given to all high school juniors. Scores in Alabama and nationwide dropped during and following the pandemic. In Alabama, performance is improving, though still below pre-pandemic highs. A full exploration of the Alabama ACT scores can be accessed in PARCA’s previous post, Alabama High School Class of 2024 Improves on ACT.

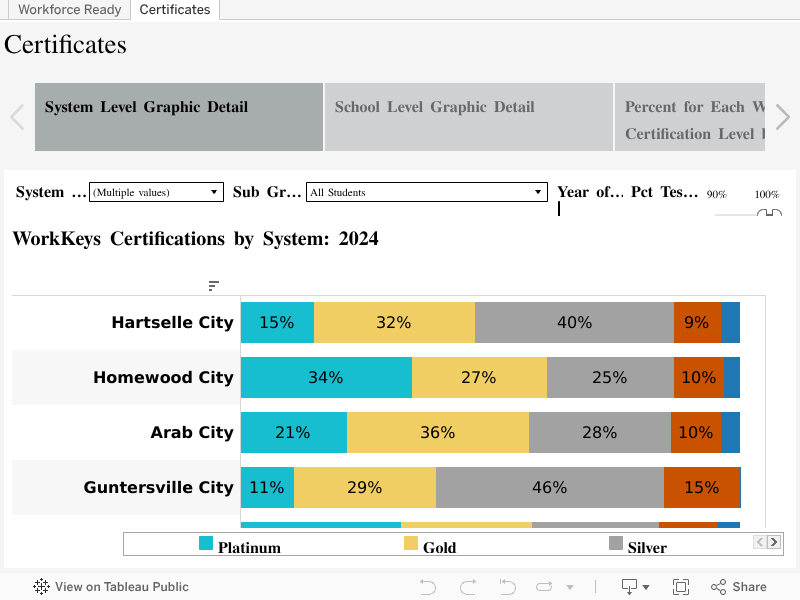

WorkKeys

ACT also produces a second standardized test, WorkKeys, through which students can demonstrate college and career readiness. WorkKeys is designed to test reading and math skills as they are applied in the workplace. WorkKeys is given to seniors and is optional. Students who score high enough on WorkKeys to earn a silver, gold, or platinum certification are considered adequately prepared to enter the workforce.

Some employers use WorkKeys as a factor in hiring decisions. The visualization below allows you to explore WorkKeys results in terms of certificates earned and trends in the number of students tested. However, bear in mind that different schools use the test differently and give it selectively, so comparisons between schools and systems can be misleading.

Explore Further

Using the tabs and menus in the visualization tools, you can explore results for your local system or school. For best results, use the full screen option to display the visualization. That button can be found on the bottom right of the visualization, next to the share button.

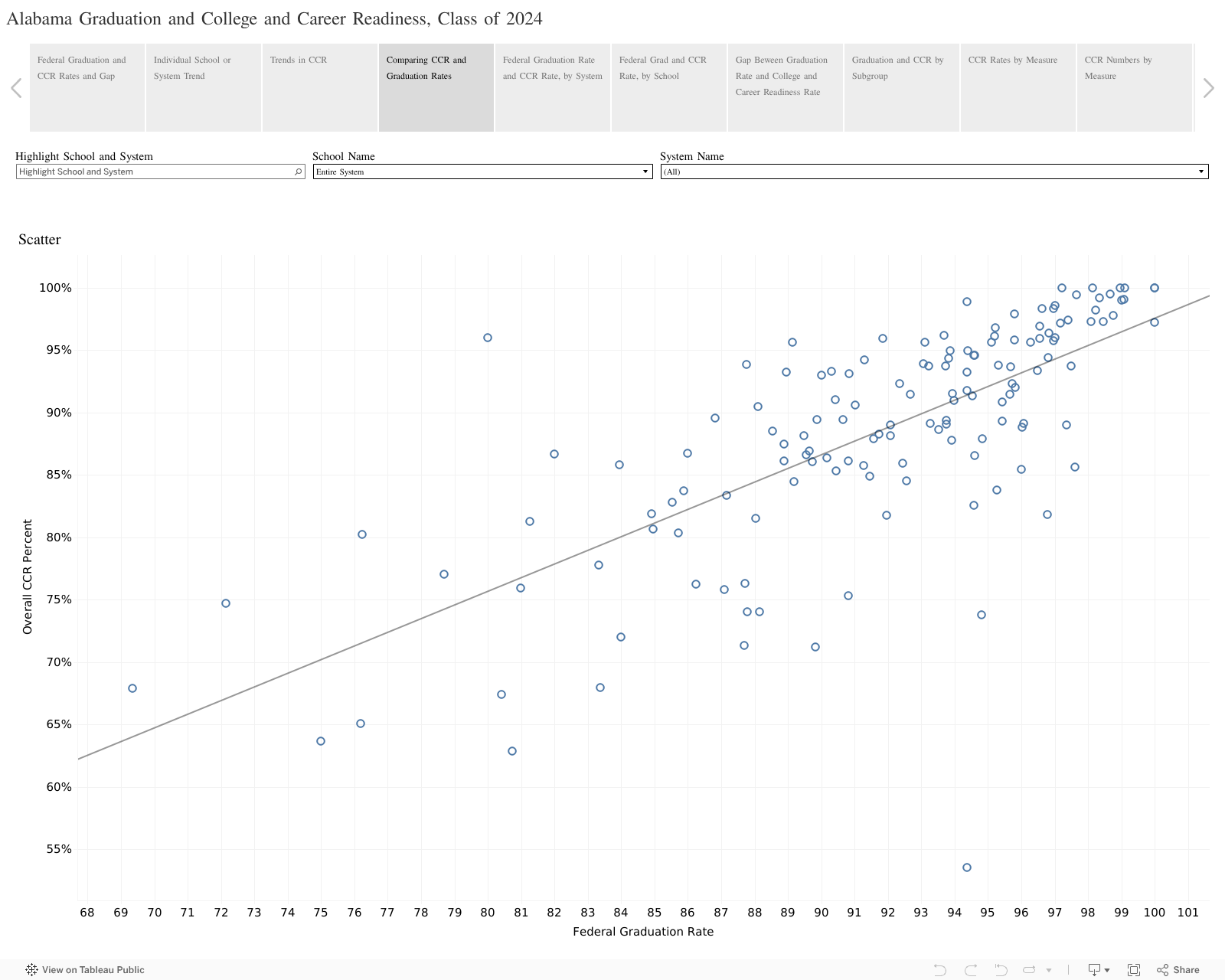

Bear in mind that some schools may have college—and career-ready rates that exceed graduation rates. This occurs when more seniors achieve one of the measures of college and career readiness than earn a diploma.