Mississippi’s Progress Not a Surprise; It was Part of a Plan

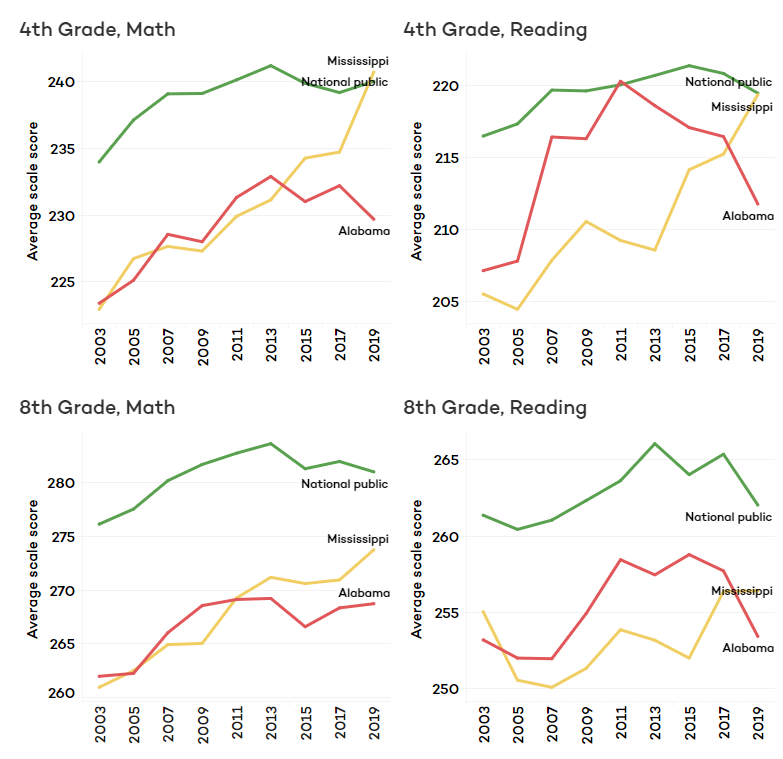

When the 2019 results of the National Assessment of Educational Progress (NAEP) were released last week, the good news was that fourth-grade students in our neighbor state, Mississippi, scored at the national average in both reading and math and that eighth graders there made significant gains in reading and math as well.

On all four measures, the average score for Mississippi students exceeds those of Alabama students, despite Mississippi’s higher level of poverty and higher percentage of students of color. The interactive chart below traces the average scale scores for Alabama and Mississippi students on the NAEP since 2003 on each of the four measures. The green line represents the average of public school students nationally. Other tabs in the chart allow you to explore other ways of looking at the data, including comparing demographically similar groups of students across states. In each of the main demographic and economic categories, Mississippi students are outperforming Alabama’s. The NAEP reading and math assessments are given every two years to a sample of students in each state, the sample representing the demographics of the state. It is the same assessment from year to year, and it is administered nationally. Known as the Nation’s Report Card, NAEP serves as the principal national measure of academic proficiency for U.S. education.

Mississippi has had a consistent and cohesive educationally-focused leadership in the Governor’s office, the State Legislature, and at the Mississippi Department of Education. Current superintendent Carrie Wright was recruited in 2013 from a leadership position in the District of Columbia’s rapidly improving public schools. Under Wright, and with the backing of an appointed state school board, Mississippi has operated under a plan that includes goals, objectives, and clearly articulated strategies aimed at meeting those goals. To track progress on the implementation of strategies and progress toward goals, the superintendent delivers an annual update that details actions taken to advance toward those goals.

Mississippi borrowed some aspects of its approach to improving reading from Alabama’s Reading Initiative. And more recently, Alabama borrowed from the Mississippi model. Earlier this year, the Alabama Legislature adopted a Literacy Act, similar to a Literacy-Based Promotion Act Mississippi adopted in 2013. Mississippi developed its own student assessment test for grades 3-8, MAAP, which was first deployed in the 2015-2016 school year. Alabama hopes to deploy its own state-developed assessment in the spring of 2020.

Over the long term, both Alabama and Mississippi have made progress in both reading and math. However, during Superintendent Wright’s tenure in Mississippi, Alabama has had five different superintendents. The State Department of Education did develop a state plan for education, Plan 2020, in 2012, but it was never fully developed and implemented and was shelved as subsequent superintendents came and went.

Reading

In 2011, just eight years ago, Alabama enjoyed the national spotlight when NAEP was released. Alabama fourth graders scored at the national average, having made the largest improvements in the U.S. That growth coincided with and has been generally attributed to the Alabama Reading Initiative (ARI). ARI emphasized a schoolwide commitment to getting all students reading at grade level, with an emphasis on Kindergarten through third grade. ARI placed a reading coach in every Alabama elementary school and required intensive professional development to teachers on research-based approaches to teaching reading.

However, after that achievement, and in the face of a constrained budget, funding for ARI was reduced, and schools were allowed to repurpose the state-funded reading coaches for other purposes. Reading scores on NAEP began drifting and in 2019 dropped sharply in both fourth and eighth grades.

Earlier this year, the Legislature adopted the Literacy Act, which will require that third graders be able to read, or they will be held back to repeat third grade. The Literacy Act, modeled after similar legislation in Mississippi and other Southeastern states, is expected to add urgency to reading instruction and to addressing reading challenges like dyslexia. ARI’s funding was also increased by $6.5 million, though at $51 million per year, that’s still far from the $64 million it received at its peak in 2008. Education leaders say the program will be restored to fidelity.

Math

While the 2019 reading results on NAEP were distressing for the severity of the drop, the math results for Alabama students were equally disturbing. Alabama school children in both the fourth and eighth grade had the lowest average test scores in the United States. It’s a familiar position for Alabama. Alabama ranked behind all other states in 2015. In 2017, Alabama students climbed a couple of notches in the rankings, but slipped back into last this year.

The state’s strategy for addressing math is less clear. In March of 2019, Gov. Kay Ivey put on hold new math standards, which had been developed by a statewide panel of educators. Ivey postponed adopting the changes to the math course of study after some conservative groups, who are opponents of the Common Core state standards, voiced their objections. In a letter to State Superintendent Eric Mackey, Ivy asked that Alabama’s new proposed math curriculum be compared to the math course of study for the top six performing states on the NAEP: Massachusetts, Minnesota, the Department of Defense’s educational system, Virginia, New Jersey, and Wyoming.

Considering Mississippi’s results, its approach to math should be examined as well. Mississippi did adopt the Common Core standards. Judging by national results, it safe to say that Common Core did not cause NAEP scores to leap. But it’s also true that states that did not adopt the Common Core have seen declines on the NAEP as well. Other factors may be contributing to an overall stagnation in educational progress. However, with Mississippi bucking the trend, Alabama would be well served to take note and inspiration from our neighbor’s progress.

Another Year of Strong Growth in Alabama Tax Collections

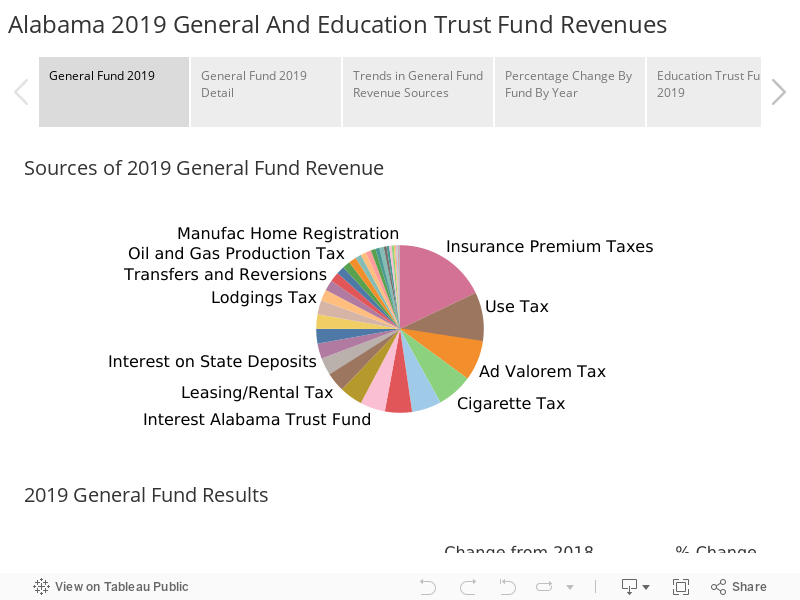

The thriving economy produced another year of surging tax collections for Alabama’s General Fund and Education Trust Fund (ETF), the two primary accounts that provide state funding for government operations. The better-than-projected results put the state in a good position to meet current obligations and weather a downturn should it arise.

It also appears that budgeting changes made by the Legislature in recent years have created more balance in revenue growth between the two funds.

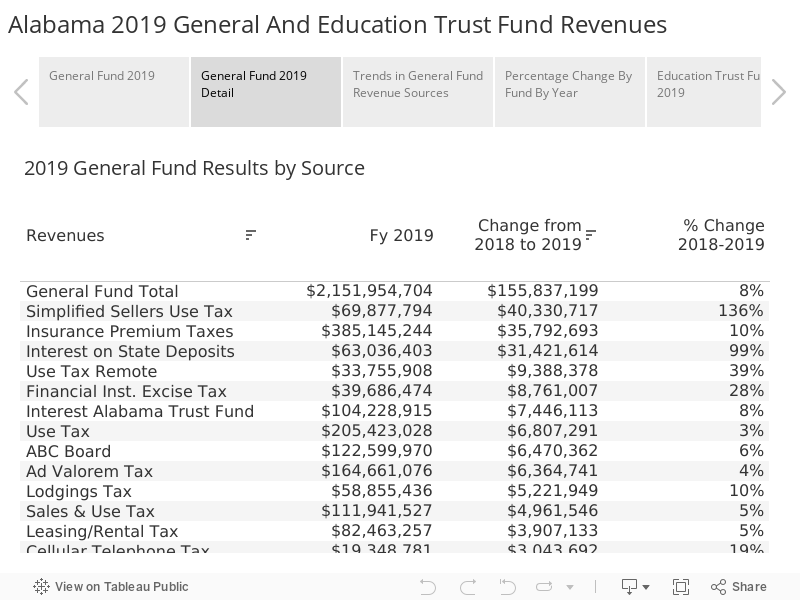

According to the state’s financial reports for the fiscal year that ended on Sept. 30, the taxes and revenues that feed the General Fund were up 8% over 2018. Revenue to the ETF increased by 7% over the previous year. It is unusual that the General Fund’s rate of growth exceeded the ETF’s. Historically, the ETF, which contains major growth taxes like the income and sales taxes, grows faster than the General Fund.

In dollar terms, General Fund revenue increased by $155,837,199.45

to a total of $2,151,954,704, while ETF collections rose by $461,710,824 to $7,215,276,202.89.

Collections in both funds exceeded projections.

General Fund

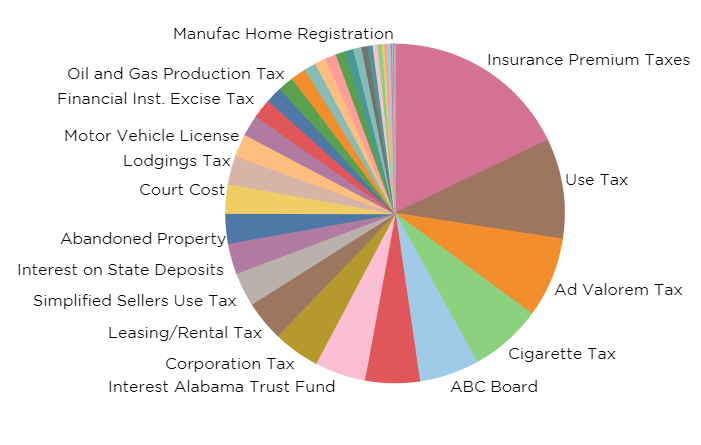

Alabama’s General Fund revenues are derived from a hodgepodge of taxes, most of which moved in a positive direction. General Fund spending supports health programs, like Medicaid and the Departments of Health and Mental Health, as well as law enforcement, the judicial and corrections system and other public safety agencies, plus a variety of other non-education programs.

In dollar terms, revenues from insurance premium taxes are the biggest contributor to the General Fund, providing $385 million or 18% of total collections. Those taxes, which are applied to the premiums paid by insurance policyholders, grew 10 percent over 2018, putting an additional $35 million into the General Fund.

There may be several reasons why this tax is growing at a faster rate than the overall economy. Since more people are employed and have more stable resources, more of them might be buying insurance in contrast to tougher economic times. At the same time, insurance companies may be charging more in premiums as they rebuild reserves needed to cover storm events and rising costs.

The Insurance Premium Tax is set to become an even bigger contributor to the General Fund in future years. A fixed amount of the tax, $31 million, had flowed into the Education Trust Fund. That division of the tax will end, and the total tax will flow into the General Fund. However, the transfer of this revenue comes with the understanding that the General Fund will have to cover the cost of the ALL Kids Children’s Health Insurance Program in future years, an expense that will rise over time.

In percentage terms, the tax that experienced the biggest jump in both its contribution to the General Fund and its rate of increase was the Simplified Sellers Use Tax. This is a tax paid on purchases made over the Internet and delivered to Alabama. Originally established in 2015 as a voluntary method for out-of-state sellers to remit sales tax to the state, the law has been increasingly tightened to require businesses that have significant online sales to participate. A 2018 decision by the U.S. Supreme Court, known as the Wayfair decision, gave further authority to collect taxes on online sales.

As more online retailers came aboard in 2019, General Fund revenue from the source jumped by 136% or $40 million to a total of $70 million for 2019. The General Fund gets 75% of the Simplified Sellers Use Tax. The remaining 25%, amounting to $23 million in 2019, went to the Education Trust Fund. So, the total revenue from the Simplified Sellers Use tax in 2019 rose to $93 million compared to $40 million the year before.

Growth in this tax will likely continue as online sales continue to rise, but the rate of increase should not be nearly as high in the future.

Also helping boost the General Fund were higher interest rates. The interest paid to the state on its cash deposits jumped by $31 million in 2019 to a total of $63 million. Interest rates have subsequently fallen so this revenue source may not be as robust in 2020.

The Use Tax, the General Fund’s second-largest source of revenue, saw a respectable 3% growth, bringing in an additional $6.8 million for a total of $205 million. The Use Tax is collected on out-of-state purchases or leasing of equipment or machinery.

Revenues contributed by the state-regulated alcohol sales were up by 6.5% to $123 million. Property taxes were up 4% to $165 million. The lodging tax jumped 10% to $59 million. Analysts believe a strong year at Baldwin Counties beaches provided a boost, assisted by increased tourism to Montgomery with the opening of the National Peace and Justice Memorial.

Some tax sources declined. Cigarette taxes continued their long slow decline, down 4 percent or $5.6 million. Still, cigarette taxes, which contributed $149 million in 2019, are the 4th largest tax source in the General Fund. Tax collections on vaping products increased 62% but are a very small source of revenue at $2.3 million for the General Fund in 2019.

While the $19 million contributed by the Cellular Phone tax appears to be an increase, base collections actually declined in 2019. The total collections for 2018 were depressed by a refund of the tax paid out as a result of a lawsuit. For the most part, mobile telephone companies no longer charge customers for calls but instead charge for data. Calling plans are taxed; data plans are not subject to tax.

Taxes on automobile titles dropped 6% after several years of gains. The decline could indicate a slowdown in auto sales, a development that would introduce a dark cloud to Alabama’s otherwise sunny economic horizon.

In the interactive chart below, you can compare trends in taxes since 2015. The menu on the right of the chart allows you to decide which taxes appear in the view.

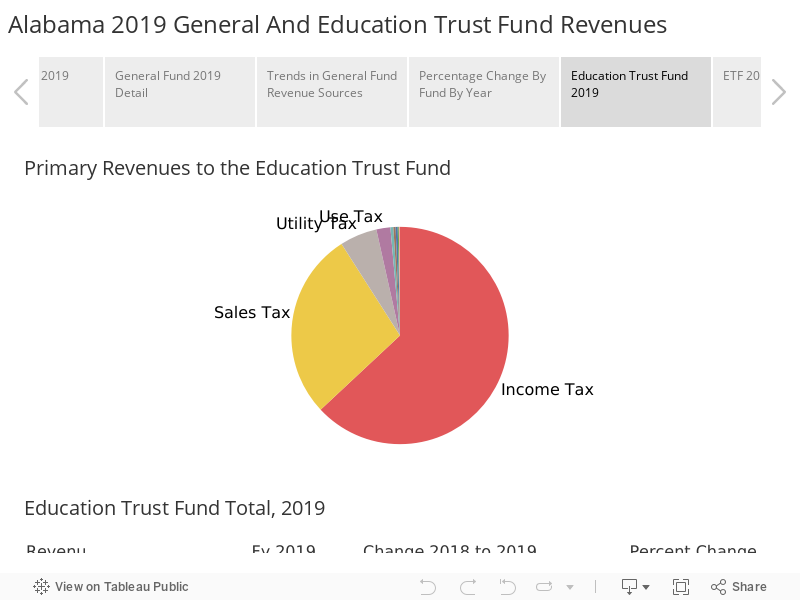

Education Trust Fund

Strong growth in income and solid sales tax growth powered another year of growth in the Education Trust Fund. Those two taxes, both of which are earmarked for education, supply over 90 percent of the education budget. In 2019, income tax collections made up 63% of ETF deposits, while sales taxes contributed 28%.

Income taxes were up $340 million, or 8%, for a total of $4.5 billion. According to financial reports, individual income tax receipts were up 6%, while corporate income taxes increased 15% over 2018. When refunds are taken into account, individuals paid $4.2 billion and corporations $455 million in income taxes.

Along with the general economic growth, the sharper rise in corporate tax collections was likely spurred by the cut in federal corporate income taxes, enacted in December of 2017. Federal income taxes are deductible from Alabama income taxes. With corporations paying less in Federal income taxes, that meant corporations kept a greater share of profits, leaving more corporate income for Alabama to tax.

Sales tax collections rose 6%, to $2 billion, contributing an additional $105 million to the ETF. Total sales tax receipts increased 4%, while the amount held back to pay state agencies decreased. The Department of Human Resources received a smaller sales tax refund because DHR is paying out less in SNAP benefits. The Alabama Department of Revenue also decreased the amount it assessed the state for sales tax collection.

Beyond the income and sales taxes, as noted above, the ETF portion of the Simplified Seller’s Use Tax grew by 136%. In the case of the ETF, that provided an additional $13 million for a total contribution of $23 million. The third-largest contributor to the Education Trust Fund is the utility tax, which brought in $401 million, which was a $5 million or 1% increase over 2018.

Implications of Better-than-Expected Growth

According to Finance Director Kelly Butler, the General Fund ended with a $275 million balance that will be available to appropriate in future budgets.

For the ETF, it’s a little more complicated, due to rules set up under the Rolling Reserve Act, a budgetary control measure designed to curb unsustainable spending and to generate a cushion for use during economic downturns.

According to Butler, the ETF generated an “overage” of $579 million in 2019. Of that, $66.5 million, or 1% of direct budgeted spending in the ETF, will be shifted to the ETF’s Budget Stabilization Fund.

The remaining $512 million will be shifted into the Advancement and Technology Fund. That money will be available for appropriation during the next legislative session to K-12 schools and colleges and universities for spending on non-recurring expenses such as deferred maintenance, school security measures, and educational technology or equipment.

The 7% growth rate for the 2019 ETF will be added to the calculation of the Rolling Reserve’s built-in cap on the growth of education spending. That budget cap is calculated by taking the ETF’s growth rate in each year of the past 15 years, dropping the year with the lowest growth rate, and then finding the average rate of growth for the remaining 14 years.

Despite the good results this year, that overall average will be down slightly. Thus, the allowed rate of growth in spending will be slightly lower in the 2021 budget than it was in the 2020 budget.

That’s because the year dropped from the 15-year window, 2004, was one of the extremely high growth years that preceded the Great Recession. In those years, recurring revenues to the ETF were increasing around 10 percent per year.

The average growth rate will be declining for the next couple of years as those high-growth years drop out of the calculations.

While a final calculation hasn’t been made, it is expected that the spending cap on the 2021 Education Trust Fund Budget will be somewhere between $300 and $400 million over the 2020 Education budget, which totaled $7.1 billion.

It’s important to remember that the Rolling Reserve Act creates a cap on increased spending. The Legislature is in no way obligated to spend up to the cap.

The Bigger Picture

Both the $2 billion General Fund and $7 billion Education Trust Fund are only part of the picture when it comes to paying for the operation of state government agencies. Beyond the tax sources detailed above, other state taxes are earmarked for certain purposes and sent directly to a designated agency.

There are also huge inflows from the federal government, particularly supporting Medicaid and other health programs, road construction and maintenance, and education. The federal contribution is a similar amount to what is generated by state taxes.

Other state agencies generate revenue. Colleges and universities charge tuition. Hunters and fishermen buy licenses that help fund the Department of Conservation and Natural Resources. Companies buy permits that help pay for inspections by the Alabama Department of Environmental Management. Those federal and state revenues are then spent supporting the agencies.

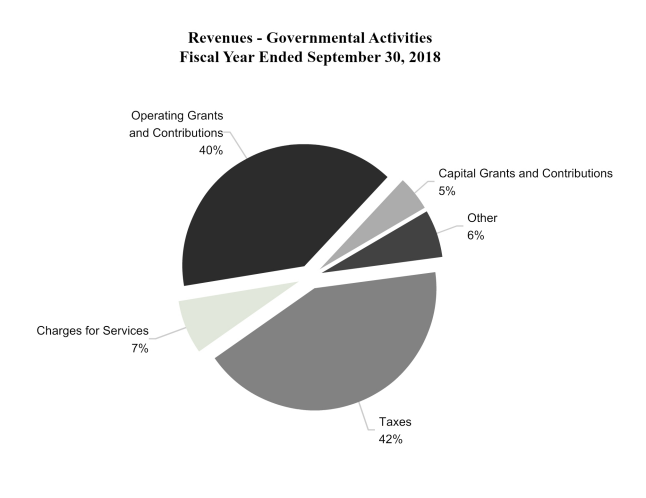

Alabama’s most recent Comprehensive Annual Financial Report (CAFR) details revenues and expenditures for Fiscal Year 2018. In terms of revenue, the CAFR indicates that total revenue was a little over $22 billion, more than double the tax collections deposited into the ETF and General Fund. The CAFR provides the chart below to illustrate the sources and proportion of all the revenues supporting the state governmental activities.

Source: Alabama 2018 Comprehensive Annual Financial Report, State Comptroller’s Office

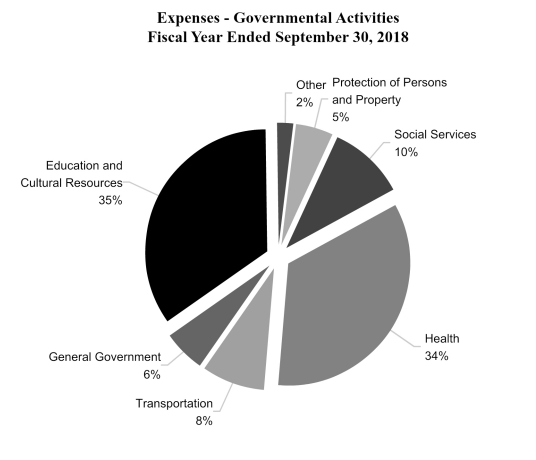

The CAFR also presents the government’s expenses for 2018, broken down by category of spending. On the surface, comparing the sizes of the General Fund and the ETF, it appears that we spend significantly more on education than we do on other functions of government. However, when federal funds and other earmarked taxes and revenues are taken into account, there is a more equal distribution of spending, with about one third spent on education and culture, about one-third spent on health, and one third spent on other functions: roads, law enforcement, the courts, prison, general government.

Source: Alabama 2018 Comprehensive Annual Financial Report, State Comptroller’s Office.

Cooperating for the Sake of Self-interest

Hoover Mayor Frank Brocato speaks to fellow mayors and Jefferson County Commissioners as they prepare to sign Good Neighbor Pledge, a non-poaching agreement forged by Jefferson County’s mayors.

Any effort to promote cooperation between governments quickly

runs into skepticism.

Cities and their citizens are self-interested, the thinking goes. They are not going to give up their advantages. They’re not going to be charitable to a neighboring community, just for the sake of being nice.

And

the skeptics are right.

However,

that doesn’t foreclose opportunities for cooperation. In fact, self-interest is

the starting point for cooperation.

That’s one the lessons learned on the way to the Good Neighbor Pledge, an agreement signed earlier this year by about two dozen mayors in Jefferson County. Under the agreement, mayors pledged not to encourage or incentivize the relocation of local businesses from neighboring cities to their own. In so doing, the mayors hope they’ve solved a problem all of them were facing: a growing demand and expectation that local governments provide tax incentives to retain or attract businesses.

On the surface, signers of the

Pledge appear to be giving up advantages and competitive tools in economic

development. However, because almost all the key governments participated, the

pledge resets the rules of the game, short-circuiting counter-productive and

mutually damaging competitive battles that were costing all cities time,

attention, and tax dollars while providing no net benefit to the region.

This feature is part of an occasional series on creative cooperation between local governments and other civic partners. Through the series, we hope to identify, share, and spread best practices and lessons learned.

The opening text of Jefferson County Mayors’ Good Neighbor Pledge

Laying the Groundwork

The Good Neighbor Pledge grew out

of an effort by the Community Foundation of Greater Birmingham (CFGB) to understand

regional challenges and to identify options for addressing those challenges. If

not for the background research and dissemination of the findings, the Good

Neighbor Pledge likely would not have come about.

After arriving in Birmingham in

2014, CFGB president and CEO Chris Nanni kept hearing from Birmingham-area

leaders that the fragmented nature of the region, 35 municipalities in

Jefferson County alone, was interfering with the region’s ability to

effectively address problems or pursue an over-arching vision for the

community.

With funding from a key circle of

the Community Foundation’s Catalyst donors, the Community Foundation

commissioned PARCA to research whether Greater Birmingham’s lack of cooperation

was negatively affecting its ability to compete and if so, how other cities and

metros have overcome fragmentation and moved toward a more unified approach to

community progress.

To help frame the issues and provide response and guidance to the study, CFGB formed a broadly-representative strategic advisory group of Birmingham area leaders who were consulted throughout the research process. After the report, Together We Can, was published, the leaders from that Strategic Advisory Group were also essential in carrying the information and conclusions out to the community.

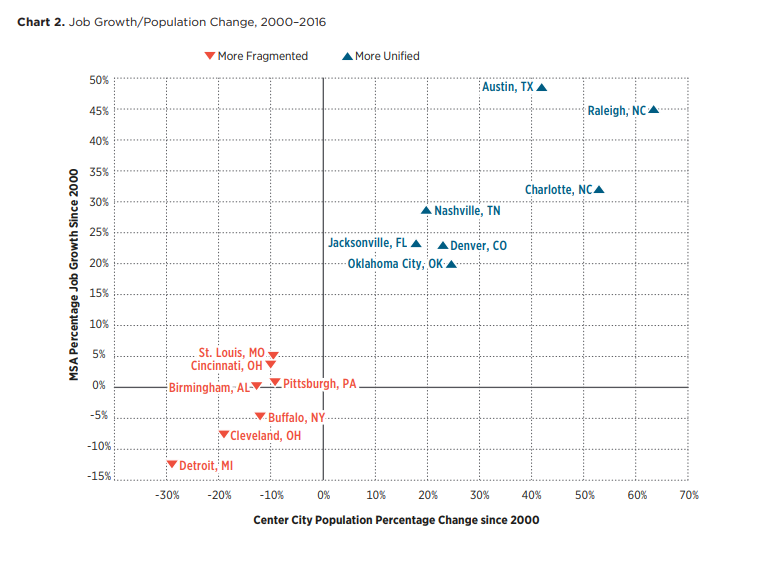

Published in June 2017, Together We Can concluded that Birmingham and other similarly fragmented cities consistently performed more poorly on economic and social measures than more unified metros. Cities around the country have long worked to overcome the challenges presented by fragmentation, and the report described four organizational models used by cities to counter fragmentation and increase cooperation.

After releasing the report, the Community Foundation and representatives of the strategic advisory group hand delivered copies to community leaders, spoke to civic clubs, and participated in radio and newspaper interviews and panel discussions. Neither the report nor the CFGB argued for a particular approach to increase cooperation. Nor was the cooperation conversation centered around a particular project or issue. It instead described approaches other cities took and encouraged Birmingham citizens and leaders to find a response that fit local circumstances.

“The education piece was

essential,” Nanni said

That neutral approach was

important because the prevailing climate among elected officials in Greater

Birmingham was suspicion. That was clear during an early presentation to the

Jefferson County Mayor’s Association.

“The first time we presented to them there was a lot of tension in the room, particularly among the incumbent mayors. For so long, the atmosphere was one of suspicion and competition. Zero trust. But as they came to see we weren’t trying to force them into something, they started warming up,” Nanni said.

The publication of the report preceded an election cycle in which several mayors’ races were on the ballot. Regional cooperation became an issue talked about in mayoral and council races that took place across the metro in 2017.

And

it just so happened that among the new crop of mayors, there were several new

faces who were open to new ways of doing things.

You Don’t Have to Reinvent the Wheel

When attempting to break old negative patterns, it is

tempting to propose starting from scratch, inventing a new organization or

governmental authority to shape a new reality.

However, it’s sometimes best to put existing institutions to work solving problems rather than inventing a new one. In Jefferson County’s case, Together We Prosper proponents looked foran existing cooperative structure that could be repurposed, energized, or motivated to drive cooperation.

The Jefferson County Mayors’ Association emerged as a candidate. It had some legal standing and functionality, but, in the opinion of many of the participating mayors, it wasn’t living up to its full potential. The mayors had a monthly meeting that was paid for by a rotating cast of lobbying groups who got an audience with the mayors in exchange for paying for their lunch. Mayors got to network and casually discuss common experiences, but there was no push to collaborate, innovate, or address common problems.

Let it be their idea

The Community Foundation encouraged and sponsored a half-day summit for the Association, during which it was hoped that the mayors could find an issue they could rally around addressing.

The Community Foundation provided a facilitator to get the conversation going, but the mayors chose the topics to explore.

So it was the mayors themselves who coalesced around a challenging initiative: ending the bidding wars for local businesses. And since they chose it, they felt ownership of the initiative.

Identify Mutual Self Interest

Local governments across the

country are waking up to the fact that offering economic incentives for local

business relocation is ultimately a losing proposition.

In 2004, communities

in the Metro Denver areas enacted a Code of

Ethics

designed to end business poaching and promote regional cooperation around

economic development. Many others have

followed suit. Just this year, Missouri and Kansas found a way to end an incentives arms

race that was allowing companies to

reap incentives by moving between the Missouri and Kansas portions of Kansas City.

According to

research, in at least 75 percent of cases, businesses would have made the same decision

to relocate or expand whether or not incentives were offered by governments.

If a business is considering equally appealing sites and they know that in the local market municipalities play the incentives game, the richer offer might make a marginal difference. However, the deal doesn’t produce a net gain for the region. The attracting jurisdiction forgoes taxes that may actually be needed to offset the increased traffic or demand for public safety protection. Granting one business tax incentives arguably gives that incoming business an advantage over existing local businesses.

Identify a Champion

To forge consensus and push the process, the Mayor’s Association needed to identify a champion. They found it in Mountain Brook Mayor Stewart Welch. Welch had only been in office two years. He came out of an investment advising and management business. He wasn’t invested in the prevailing political order of things, and he had credibility when talking about business and economics.

Welch reached out to each mayor and worked toward a proposal. The first part of the pledge was easy. The mayors would pledge not to solicit a local business located in a neighboring municipality to move.

It was harder to ask the mayors

to give up their tactical weapon.

Welch kept working to convince

his fellow mayors that a widely accepted agreement would short-circuit what

seemed to be an increasing problem. Expanding

businesses within the region were actually motivated to move across municipal

lines, because it was expected that they could get incentives to move or, when

those incentives were put on the table, they’d get an incentive offer to stay where

they were.

Welch worked to convince mayors that it was a counterproductive and unnecessary exercise to incentivize moves that were going to happen regardless. It was a losing proposition for each city and the region, he argued. It diverted resources, time, and attention that should have been spent on bringing in businesses from outside the region, a business that would result in a net gain in employment and population for the region.

Do your Homework

While the initial report included

a description of the Denver area’s no-poaching Code of Ethics, the Community Foundation

provided Welch and the other mayors with additional research support. They

helped locate five other similar agreements from around the country and arranged

phone conferences between mayors and the individuals in Denver who were involved

in crafting the no-poaching agreement there. The mayor of Birmingham provided a

staff member’s assistance with the drafting process.

Welch began circulating drafts, and with the other

mayors’ input, they moved toward mutually agreeable language. And they came up

with a catchy name: “The Good Neighbor Pledge.”

Declare Victory

Eventually, 23 cities agreed to sign on, including the eight largest. In sum, the signatories represent about 85 percent of the county population. Even though three sizable suburbs — Irondale, Fultondale, and Gardendale — declined to sign, the “coalition of the willing” moved ahead.

The mayors gathered at the Jefferson County Courthouse to formally sign the agreement with the Jefferson County Commission looking on. The event drew favorable press coverage and continues to inspire further conversation about additional cooperative ventures.

Success Begets Success

The Good Neighbor Pledge is not a

legally binding agreement. It doesn’t have “teeth.”

The mayors are still working on a dispute resolution process that could handle conflicts over the Good Neighbor Pledge if they were to occur.

Going forward, the mayors have discussed increased cooperation on 9-1-1 services. They’ve also discussed creating a comprehensive countywide or even regional listing of available office and commercial space and industrial parks.

Regardless of what is next, it is hoped that the mayors have taken a step toward communication and cooperation in a local landscape that has traditionally been marred by distrust and competition. And they continue to look out for self-interested opportunities to help improve conditions for all.

Local Government 3.0

Montevallo Mayor Hollie Cost explains the function of Owl’s Cove Park, a part of the broader downtown revitalization and partnership project with Shelby County and the University of Montevallo.

The following feature, which describes an alliance between the City of Montevallo, The University of Montevallo (UM), and Shelby County, marks the launch of an occasional series on creative cooperation between governments and other civic partners. Through the series, we hope to identify, share, and spread best practices and lessons learned.

Why We’re Writing This

Neighboring communities are inextricably linked in metropolitan or regional economies. Traditional ways of operating can lead to siloed thinking, inefficiencies, and, in some cases, counterproductive competition. Increasingly, neighboring governments and agencies are looking for ways to partner to achieve common interests. In recent years, PARCA has engaged in studying issues of municipal fragmentation and efforts to overcome its effects through cooperation among local governments in Greater Birmingham and in north Alabama’s Shoals region.

In April 2019, Greater Birmingham saw progress on cooperation with the crafting and signing of a Good Neighbor Pledge by members of the Jefferson County Mayors’ Association. Developed with the support of the Community Foundation of Greater Birmingham, the Pledge seeks to increase trust and prevent incentive bidding wars between local municipalities over business relocations.

Meanwhile, the Committee for A Greater Shoals used PARCA’s report on its local government landscape to launch an array of civic improvement working groups, involving hundreds of citizens. Those working groups have now identified opportunities for further progress on intergovernmental cooperation, joint efforts on tourism, digital infrastructure upgrades, and increasing investment in higher education and training.

Montevallo’s Shared Investment in Shared Vision

Cooperative efforts in Montevallo between the county, the city, and the university which have been brewing for a decade, have in recent year produced a significant transformation.

For most of its history, Montevallo (current population 6,674) has been a trading center for the surrounding area. Area residents have worked at the university and local schools, in some small-scale manufacturing, in coal mining, timber, and in farming. If you visited Montevallo about a decade ago, you would find a typical Alabama small-town downtown, going through the usual struggles such towns face as retail and travel patterns shift to Interstate corridors.

Meanwhile, the university was something of a separate bubble. Founded in 1896, as the Alabama Girls’ Industrial School, the school grew into a respected college for women, and, after going co-ed in the 1950s, was re-christened the University of Montevallo in 1969. UM evolved into an unusual school: a public college, but one with qualities of a private college, due to its small class sizes and liberal arts concentration. While the university was obviously important to the town as an employer, there was an odd sense of separation from the downtown, despite the fact the two were only a few short blocks apart. Students tended to commute rather than live and spend in town.

Now, the lines between town and campus are deliberately blurred. The small town with a small college is beginning to have the look and feel of a “college town,” a place where campus life and energy animates the town and the town embraces and enlivens the college.

A $4 million project for reconfiguring, landscaping and repaving Main Street has recently been completed.

The downtown is updated, with new signage, lighting, and sidewalks, plus a couple of pocket parks and new greenery. What had been a long-shuttered, modernist Alabama Power office building on Main Street has been transformed into the University of Montevallo on Main, a classroom building that draws students and professors off the campus and into town for at least some of their classes. Another Main Street storefront has been renovated to serve as the University of Montevallo Bookstore.

The view of Owl’s Cove pocket park and the University of Montevallo on Main in downtown Montevallo.

On the edge of campus closest to downtown, a $25 million, 36,000 square-foot Center for the Arts building is rising. According to the University, the Center will include a 350-seat theater with state-of-the-art acoustics and technology for music concerts and theater performances, a 100-seat black box theater, and a courtyard suitable for outdoor performances and receptions. The building is expected to build on UM’s traditionally strong arts and theatre program, while also serving as a venue for drawing events and competitions from K-12 schools throughout the year.

The blocks between downtown and the University of Montevallo campus have been reworked with sidewalks and landscaping, an inviting pedestrian connection. The wrought iron gates to the university are open wide, and from them, a University of Montevallo purple “Welcome” banner hangs.

A new $25 million University of Montevallo Center for the Arts is rising at the edge of campus near downtown.

New sports venues have been added, strategically placed to intermix the college and the town. A new women’s softball field was built on city property across Main Street, adjacent to K-12 schools and the public library. Meanwhile, the school’s running track, developed with investment from the county, is open for use by the Montevallo public.

Blurring the Lines between Town and Campus

This mixing of university and town life is deliberate. It flows out of a strategy developed by the partners to bolster the University of Montevallo, the town’s biggest asset and one of the largest employers in Shelby County, and to build it into a more productive engine for the town’s economy and culture.

Big employers are valuable in Shelby County. The county is one the most affluent and fastest-growing in the state, but about half its residents work outside the county. UM employs almost 500 full-time employees with gross wages for non-student employees totaling $29.35 million in 2018. Campus and dining operations employ another 70, approximately 40 full-time, with gross wages of around $1.5 million.

Even before the three-way collaboration came about, Shelby County, recognizing the strategic importance of the University, began investing lodging tax revenue in University projects that would help the university recruit and retain students. Shelby County uses its lodging tax revenue to promote tourism and economic development. In those investments, the county looked for projects that would provide benefit to the local community as well.

A comprehensive plan for the City of Montevallo, developed in 2008, sketched a vision of a revitalized downtown, complete with interconnection to the University. However, progress toward realizing that vision began in earnest in 2012, with the City’s passage of a 1 cent sales tax and with the formation of a Montevallo Development Cooperative District (MDCD). Organized as a Capital Improvement Cooperative District under AL Code § 11-99B (2016), MDCD is a partnership between the city, the county, and university. MDCD can act like a corporation. It can buy, sell, or lease property, and enter into contracts.

The City of Montevallo pledged 90 percent of the revenue from that 1 cent tax to the MDCD, which, in turn, used that pledged revenue stream to issue $5 million in bonds. Overall, the city has invested about $6 million through the MDCD, about $1.75 million in joint projects and $4.25 million in city projects including paving, relandscaping, and the construction of a new city hall. Both within and outside the MDCD, the county has invested $4.5 million with another $900,000 pledged for projects now underway. Meanwhile, the University of Montevallo is providing $21.7 million of the funding needed for the new Fine Arts Center and has invested more than $1.1 million in other projects with MCDC and the county. Investment by local partners on transportation projects also drew in close to $5 million in federal funding.

Not every project flows through the MDCD and not every MDCD project involves more than one partner, but the District keeps communication constant between the partners, and when one or more of the partners want to engage in a joint venture, the mechanism is there and waiting. It also serves as a vehicle for operating ongoing cooperative ventures like the jointly-owned buildings Montevallo on Main and The Main Street Tavern, another MDCD-restored building now leased to a restaurant.

Main Street Tavern operates in a building restored and leased out by the MCCD.

The public investment has spurred private interest and investment. A Montevallo chapter of Main Street Alabama has been formed, supported by local businesses. That group has spearheaded a grant program that has repainted building facades in the historic core of storefronts. Some of those storefronts are occupied with businesses new and old, and some are in the midst of cleaning or restoration. They share Main Street with chain stores like McDonald’s, KFC, Taco Bell, and CVS, but the chains have new urban signage and design, which blend better with the appearance of the historic core.

Dee Woodham, a former Montevallo councilwoman who continues to serve as Montevallo’s representative to the MDCD, said the vision for a revitalized college-oriented Montevallo formed over a decade ago, but it was not until the county, the city and the university joined together and committed resources to the vision that things started to happen. “This is an impactful way of doing nice things in a small town,” she said.

Challenges

The investments made at UM and in Montevallo are not just feel good improvements. They are strategic responses to challenges. All parties recognize that the University of Montevallo has been, and will be, facing stiff competitive headwinds.

In the early 2000s, the University of Alabama launched an aggressive effort to grow its enrollment from 20,000 to its current total of over 38,500. Colleges and universities across Alabama felt the effects of UA’s well-resourced recruitment efforts, sparking increased competition for in-state students.

And because the rising generation is smaller and because the state hasn’t seen much in-migration, the pool of in-state, college-age students has been relatively constant and may actually decline in coming years.

While the University of Montevallo’s historic dedication to the liberal arts is a selling point, the current fashion in higher education, considering the cost of college, is to emphasize programs that more obviously and directly lead to careers. UM’s annual tuition and fees of over $13,000 are the highest among Alabama public colleges. However, its 13 to 1 student to faculty ratio is lower than any Alabama public college, and its tuition is lower than the private liberal arts colleges with whom it competes.

The University’s current enrollment of about 2,600 is down from about 3,000 several years ago.

With pleasantly landscaped promenades now connecting downtown and campus, the walk between the two is much more inviting.

Responding to Challenges

As a recruitment tool and to broaden its appeal, the University is adding sports teams, with the county aiding in that investment. The county helped develop the lacrosse field, allowing UM, which participates in NCAA Division II athletics, to become the second public university in Alabama to offer men’s and women’s lacrosse. That’s a draw for both in-state and out-of-state students who want to continue playing in college and don’t have many options in the Deep South.

The county also helped with the construction of a stadium for women’s softball, which was built on land provided by the City of Montevallo.

The University has also expanded other sports offerings hoping to attract scholar-athletes. It added a swimming team, taking advantage of an existing Olympic-sized pool at the student center.

On the slightly offbeat note, UM has a nationally-ranked collegiate bass fishing team, taking advantage of Montevallo’s proximity to the fertile lakes of the Coosa chain. UM also added an “Outdoor Scholars” program to showcase its proximity to the Black Belt’s fishing and hunting grounds.

And starting this fall, UM will field a competitive eSports team, with the aim of recruiting students who are interested in electronic gaming, in particular, a game called, League of Legends.

While UM’s investments haven’t yet produced a surge in enrollment, the University believes it has positioned itself for growth through its recruitment efforts, expansion of sports, and other investments like the Fine Arts Center and a new home for its School of Business. And the joint investments with the city have created an atmosphere more conducive to having students who will enroll in and live in Montevallo rather than commute.

Defining Goals and Expectations

For the partnership to thrive, all parties agreed that it was important to spell out their objectives, define the organizational structure, operate transparently, and come to a written understanding of expectations. The Shelby County Commission’s detailed resolution that endorsed the partnership describes underlying motivations and history of the partnership. Together, the parties agreed to articles of incorporation. Another practice followed by Shelby County when it commits to joint ventures is a performance contract, like the one adopted by Shelby County and the UM as a condition of the county’s support for the new fine arts center.

The county agrees to provide up to $1.2 million over seven years to support the project in order to aid the University’s recruitment and retention of students and the attraction of visitors to the community. But that contribution is conditioned on UM developing a schedule of events, performances, conventions, and competitions, targeting not only university students but also high school and middle school students. The University agrees to set goals for attendance, track it, and report back its results. UM has already laid out a draft calendar of more than a dozen proposed events each year through 2025. Depending on how well UM does in meeting performance expectations, the Shelby County Commission can decide to accelerate, slow down, or terminate its support to the project.

The MDCD has three members, one appointed by each entity. Within the parameters set out for it by its authorizing bodies, MDCD can operate more nimbly than a government. However, in MDCD’s case, the District functions as a public body under the open meetings law. Advance notice of meetings are posted. Decision-making takes place in public meetings. Minutes are taken and published on the web, as are financial reports and audits.

Caveats

While collaboration has clear advantages, it is not without risks.

In any partnership, questions can arise over whose interests are being served. For example, some townspeople worry that the town’s relationship with the university is too close. The mayor and two council members are university employees. A third council member is married to a university employee.

Janice Seamon, a Montevallo realtor involved in historical preservation causes, said cooperation is important and has produced positive, tangible results. But in her opinion, in any town, if the largest employer directly or indirectly employs the majority of the council, that has the potential to create conflict. “Having the major employer in control of city government is not good practice,” Seamon said.

Also, one of the virtues of the MDCD — its nimbleness and lack of bureaucratic structure — can lead to questions about accountability. Montevallo Councilman Rusty Nix points out that many of the projects that have run through MDCD are really city projects and don’t involve the other partners. Why, he asks, are these public expenditures run through MDCD, an alternative body on which the city’s representative is not an elected official? Why aren’t at least those solo projects reviewed for approval by the elected City Council?

Woodham, the former councilwoman and the current City of Montevallo representation to the MDCD, acknowledged that the potential for a conflict of interest exists with university employees serving on the council, but at the same time the town needs the interest and input from the university community. Woodham thinks that so far officials have been able to pursue mutually beneficial projects under terms fair to all parties. Ultimately, voters will pass judgment on that.

As for her representation of the city on MDCD despite no longer being an elected official, that’s up to the city council. Neither the county nor the university representatives are elected, but all are accountable to their appointing authority.

Measuring Success

The partnership effort of the county, the university, and the city has already achieved undeniable results. Time will tell to what extent success will fully flower.

The City of Montevallo is showing population and revenue growth, above and beyond the extra revenue produced by the increased sales tax rate. The accumulation of improvements is creating a sense of new possibilities. There are still vacant storefronts to fill, but almost two dozen new businesses have opened in the past three years, including a bakery, a bar, a cake and coffee shop, a Taco Bell, and a popsicle shop. Coming later this fall, Slice Pizza plans to open in Montevallo, its third location in the metro area.

At the same time, the aggressive changes at the University of Montevallo have not yet yielded a surge in enrollment. UM is well short of its Fall 2019 goal of 3,000 undergraduates. Officials hope that as the new sports teams become established and as UM’s new full-time student recruiters in Georgia and Tennessee spread the word, interest and enrollment will gather steam and the investments made by the partners will pay long-term dividends for all parties.

This partnership may be a model that other colleges and communities in our state can explore.

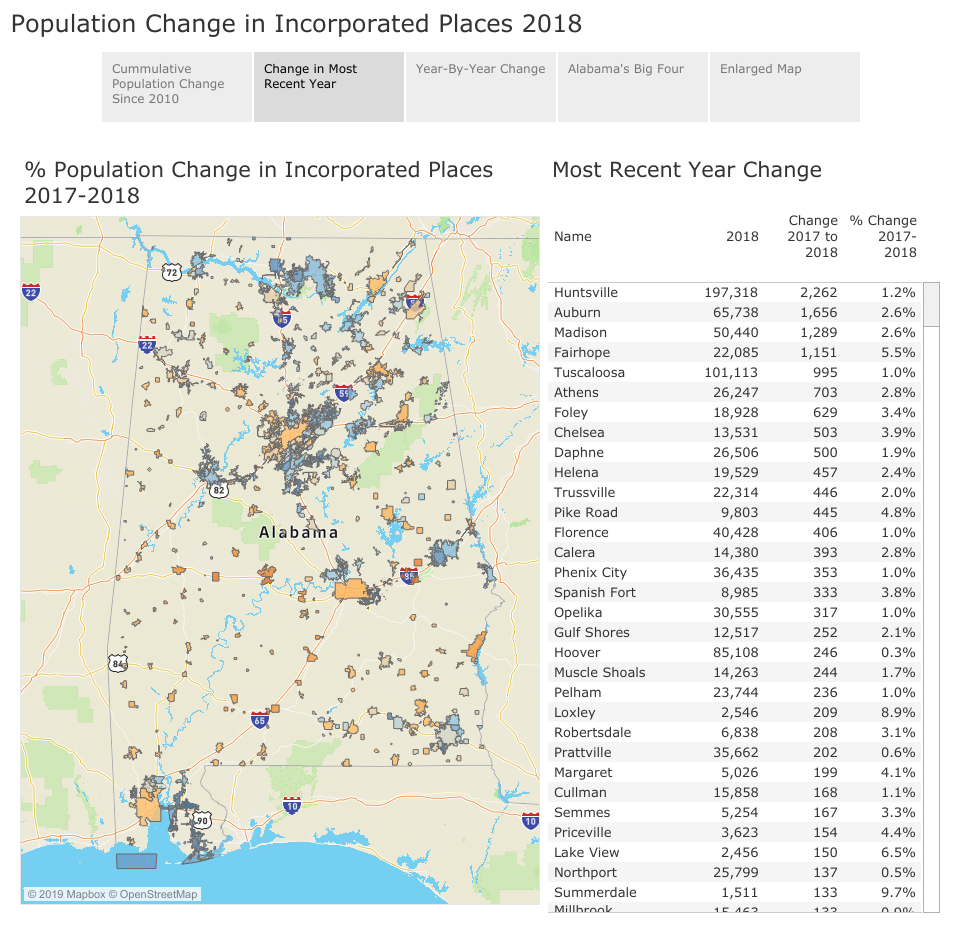

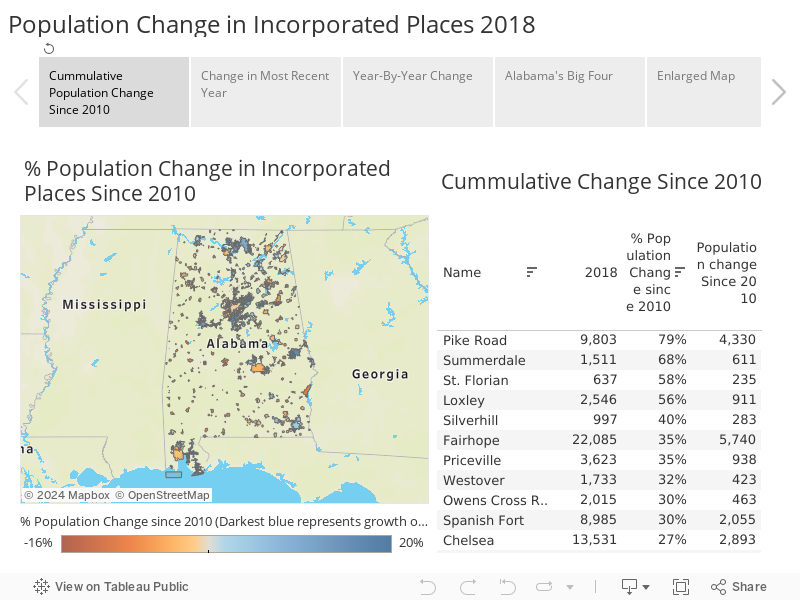

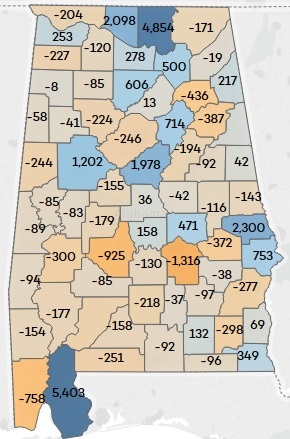

Population Change in Alabama Cities 2018

Huntsville continues its trajectory towards becoming Alabama’s largest city, while Birmingham, Montgomery, and Mobile continue to drift lower, according to the most recent city population estimates released by The Census Bureau. The two major college towns Auburn and Tuscaloosa continue to grow, as do several cities in Baldwin County.

The new estimates cover the time period between July 1, 2017, and July 1, 2018, and also look back to 2010, the year of the last official Census. Data from the same time period has already been released for state level, metro areas, and counties, and PARCA has published analyses and interactive tools exploring that data. The new cities data is below. Use zoom and drag tools to explore a particular area. Use the button in the bottom right corner if you want a full-screen display.

Huntsville and North Alabama

The city of Huntsville added more residents than any other Alabama city with an estimated 2,262 gain in 2018. If current trends continue, Huntsville (197,318) will surpass Birmingham (209,880) as Alabama’s largest city within the next several years. However, Birmingham’s metropolitan area population (1,151,801) is more than twice as large as Huntsville’s MSA (462, 693).

The Huntsville suburb of Madison ranked third in numeric gain adding 1,289. Huntsville has avoided the dilemma faced by many center cities: becoming hemmed in by and losing population to newer suburbs. In fact, Huntsville, through strategic annexation, has now completely surrounded Madison. While Madison can continue to add residents in its current footprint, it will not be able to spread out by annexing contiguous territory.

Though Madison County cities are capturing most of the North Alabama growth, nearby Athens in Limestone County appears to be receiving some of that inflow. In the farther reaches of the Huntsville orbit, Florence and Muscle Shoals had bigger gains in population in 2018 than in any year other in the decade.

Birmingham Area

In the Birmingham metro area, the core city of Birmingham was estimated to have lost over 1,000 residents between 2017 and 2018. Birmingham has bobbed up and down through the decade, but this most recent year saw the steepest decline.

However, there is population growth south and east of the core city, and the most recent estimates indicate that growth is shifting to suburbs farther south. In the most recent year, the suburbs immediately south of core city, Homewood and Mountain Brook show slight population losses, and Vestavia a slight gain. Hoover, while it did add 246 residents, is growing more slowly now than smaller cities to the south like Chelsea (+503), Helena (+457), and Calera (+393). Meanwhile, to the east of Birmingham, Trussville added 446 residents, according to the estimates.

Montgomery Area

The estimates show Montgomery losing 1,674 residents in 2018, while its emerging suburb of Pike Road gained 445. Suburbs to the north, like Prattville (+202), Millbrook (+133), and Wetumpka (+37) saw gains, but the Montgomery metro area as a whole has seen a population outflow.

Some of the population loss in the Montgomery area may be due to the strong growth being seen in Lee County, home to Auburn University. A separate Census survey tracks residential migration across county lines. A look at that data reveals that Elmore County had a net loss of 352 residents to Lee County. Nearby Tallapoosa and Macon County, which are not officially part of the Montgomery metro area, are also losing residents to Lee County.

Meanwhile, Lee County’s two larger cities have been among the state’s biggest gainers in population, according to the estimates. Auburn is second to Huntsville in numerical gain, having added an estimated 12,000 residents since 2010. Over the same period, Opelika ranks No. 10 in the state with an estimated gain of 4,000.

Mobile Area

The 2018 estimates have the City of Mobile declining in population by 953 residents. Census estimates the city has lost about 5,000 people since 2010. Some nearby communities in Mobile County like Semmes and Saraland have gained population over the past decade, but the growth in those communities isn’t enough to offset Mobile’s population loss. One might assume that the rapid growth just across the bridge in Baldwin County is being fed by residents moving out of Mobile. However, other Census data sets indicate that isn’t necessarily the case. While there is some movement from Mobile to Baldwin County, there is also a considerable residential movement back and forth between Baldwin County to Mobile. When moves to and from the county in question are accounted for, Jefferson County had a net gain of about 500 people from Mobile County, compared to a gain for Baldwin of about 250.

Other Urban Centers and the Rest of the State

Like Auburn and Opelika, Tuscaloosa and Northport both continue to grow, though at a slower pace than the rival towns to the east. Tuscaloosa remains substantially larger than Auburn, about 100,000 vs 65,000. Opelika is larger than Northport: about 30,000 vs. 25,000.

As mentioned, Florence and Muscle Shoals showed slight growth in 2018, according to the estimates, as did Phenix City. Dothan was flat, and Anniston and Gadsden both experienced net out-migration.

A scattering of smaller towns in northeast Alabama and southeast Alabama showed population growth. However, most smaller cities in rural counties lost population. Selma was particularly hard hit, with a net loss of almost 500 people in 2018. Since 2018, Census estimates Selma’s population has declined by 2,898 dropping from around 20,000 down to 17,000, a 14 percent population decline. Small towns in Black Belt counties, cities like Tuskegee, Eufaula, and Demopolis, continue to experience population declines, but so do towns in east central and northwest Alabama like Jasper, Alexander City, and Sylacauga.

Alabama County and MSA Population Trends

The latest estimates from the U.S. Census Bureau show continued strong growth in the Huntsville metropolitan statistical area (MSA), slightly positive growth in the Birmingham MSA, and slight declines in Mobile and Montgomery metro areas. For 2018, Huntsville’s growth rate ranks No. 64 out of the nation’s 383 metro area. But Alabama’s other large metros lag behind peers in terms of percentage change in population, with Birmingham ranked No. 251 out of 383, Mobile, 324, and Montgomery, 327.

Meanwhile, only 22 out of Alabama’s 67 counties added population in 2018. Most rural counties lost population, while most counties connected to a metro area gained. However, three of the four most populous counties home to the urban cores of the major metros areas — Jefferson, Montgomery, and Mobile — experienced net losses in 2018 as outmigration to surrounding suburban counties continued. Madison County, home to Huntsville continued to gain.

PARCA has updated its interactive maps and charts that allow users to explore local population changes and trends. PARCA tools for state-level population estimates were updated earlier this year. Estimates for cities will be released this summer.

Huntsville MSA

The Huntsville’s 462,693 person MSA includes Madison County, home to Huntsville (Pop. 366,519) and Limestone County (Pop. 96,174). Madison County is second only to Baldwin county in numeric population growth since 2010, and according to the estimates it added more people than ever in 2018, an estimated 4,854 in 2018. Limestone County is now the state’s second fastest growing county in percentage terms, adding 2,098 people in 2018.

Huntsville’s growth seems to be aiding population growth in other neighboring counties outside the Huntsville MSA. Marshall County has been steadily gaining population for most of the decade and now Morgan County, home to Decatur, has turned positive according to the estimates. That has caused the Decatur MSA to break a streak of population losses stretching back several years.

Birmingham-Hoover MSA

At 1.1 million and including seven counties, Birmingham’s MSA is more than double the population of second place Huntsville’s two-county MSA. In fact, Jefferson County, the central county of the Birmingham-Hoover MSA with 659,300 residents is significantly more populous

The estimates show Jefferson County with a slight loss in 2018, down 246 people. Since 2010, the estimates show Jefferson County with a net gain of 794 residents. Population change is driven by natural increase (births vs. deaths) and migration (net domestic migration plus net international migration). Jefferson County’s birth rate exceeds its death rate so the county adds people, 14,120 since 2010. But the county has a net outflow of residents moving elsewhere in the state or the country: 18,215 more people moved out than moved in. That would set the county up for net loss in population if it weren’t for a net inflow of international migrants. Jefferson County has added 5,335 of those since 2010, according to the estimates. While international in-migration has offset population loss in Jefferson County, and in other core counties as well, levels of international migration have dropped in the last two years.

Where are the leavers going? Adjacent Shelby and St. Clair Counties experienced net positive domestic migration adding 10,368 and 3,820 respectively since 2010. Walker, Blount, Bibb and Chilton County had more people moving out to other parts of the state or country than moving in according to the estimates. Blount and Chilton offset those losses with mild gains through natural increase and international migration. Walker and Bibb did not.

Mobile

With 413,757, residents Mobile is the state’s third largest MSA and it consists of a single county, Mobile, the state’s second most populous county. The federal government determines which counties are joined together in metro areas. Mobile County lies adjacent to the state’s fastest growing county, Baldwin. Despite the obvious connections between the two counties, the level of commuting between the two counties isn’t high enough for the federal government to consider them a single metro.

Mobile county’s population dynamics mirror Jefferson, with a net outflow of domestic migrants offset by a positive natural increase and international in migration.

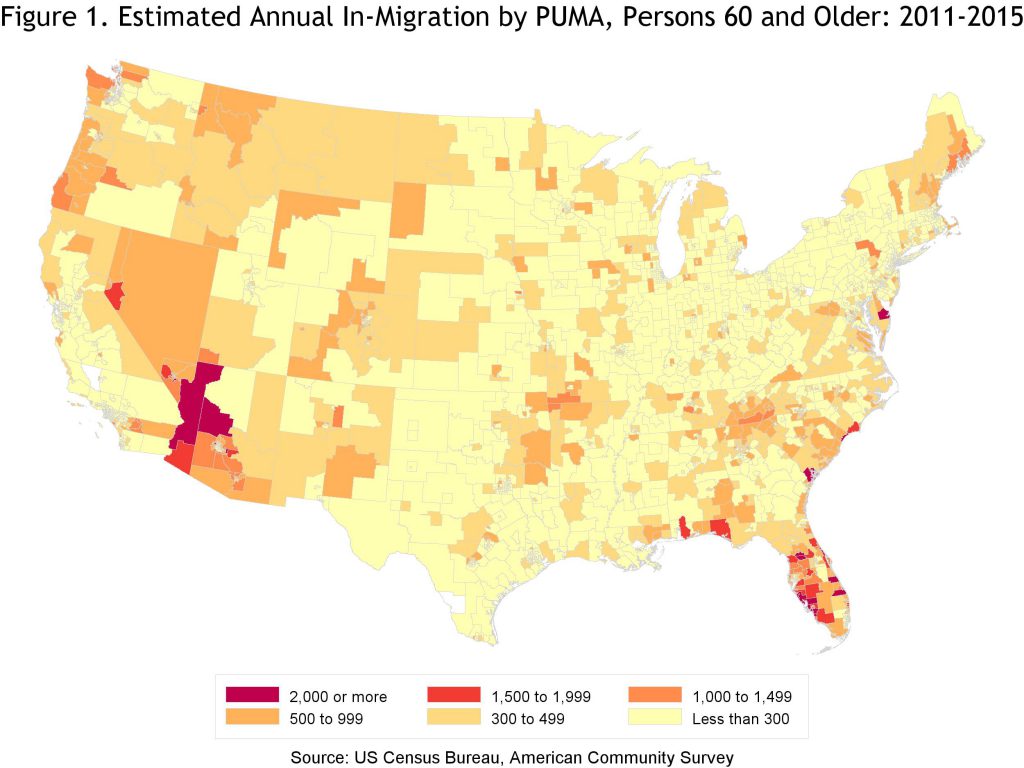

Baldwin, on the other hand, is growing, like no other county in Alabama. It has added an estimated 35,758 residents since 2010. The county is also a metro area of its own, known as the Daphne-Fairhope metropolitan statistical area. What is driving growth: heavy domestic in-migration, particularly from individuals over the age of 60.

Samford University sociology professor Don Bradley has analyzed late-in-life migration for unpublished white paper commissioned by Where to Retire Magazine. In his review of Census data, Bradley found that Baldwin County was receiving 1,798 new residents over the age of 60 each year. That ranked Baldwin among the top 30 areas in the country for receiving persons 60 and over. That same elevated growth pattern can be seen in many coastal counties from North and South Carolina, and Florida, as well as retirement hotspots in Arizona and Nevada.

Montgomery MSA

Of the major metro areas, only Montgomery has seen a net population loss since 2010. Within the metro area, Montgomery County has lost an estimated 3,615 since 2010, and the slight gains in Elmore (2,594) and Autauga (1,027) have not been enough to offset the loss.

Smaller Metros

Perhaps influencing Montgomery’s population stagnation is the draw of Lee County, also known as the Auburn-Opelika MSA. It has the second fastest rate of growth and ranks third among Alabama MSAs in numeric growth, having added 23,641 residents since 2010.

In addition to the being home to Auburn University, Lee County lies between the two Korean automakers, Hyundai in Montgomery and Kia in West Point, GA. In terms of county growth, Lee’s neighboring county, Russell, is also adding residents at a healthy pace. Russell, home to Phenix City, is considered to be part of the Columbus, GA metro area, which has seen growth over the decade. The army base, Fort Benning, on the Alabama Georgia border is a major driver of population dynamics there.

Across the state, Tuscaloosa as a county and as a metro area continues to see growth, almost all of it concentrated in Tuscaloosa County, which has added 14,243 residents since 2010 according to the estimates. Pickens County has seen a slight gain in population since 2010 but Hale County also included in the Tuscaloosa MSA, has lost about 1,000 residents since 2010.

While the Dothan MSA is off the major interstate corridors, it has continued to post modest population growth. Houston County, home to Dothan, has added 3,168 since 2010, according to the estimates, while Henry and Geneva Counties have shown slight declines over the period. Houston’s population growth stemmed from positive natural increase and positive migration.

In the northwest corner of the state, the Florence-Muscle Shoals metro area saw about the same level of domestic in-migration as Dothan. But the two counties Lauderdale and Colbert both have negative rates of natural increase, meaning that more deaths are occurring in those counties than births. Negative rates of natural increase tend to show up in places where the population is disproportionately elderly.

The two remaining MSAs Anniston-Oxford, comprised of Calhoun County, and the Gadsden MSA (Etowah County), also have negative rates of natural increase. And both those counties have negative migration rates, more people move elsewhere than relocate to those counties. Both of the counties have lost population throughout the decade.

Among Alabama counties, Dallas County, home to Selma has had the steepest losses with an estimated 5,508 loss in population since 2010, a decline of 12.6 percent. Two other Black Belt counties, Perry and Macon are declining faster than Dallas in percentage terms. Perry County lost 13.6 percent of its population since 2010 according to the estimates, while Macon County lost 14 percent.

Revisiting How Alabama Taxes Compare, 2018

With just a few hours remaining to file state and federal taxes, revisit our 2018 analysis of state and local taxes, originally published in December 2018.

Alabama’s state and local governments collect less per capita in taxes than state and local governments in any other state in the union, according to new data from the U.S. Census Bureau.

Annually, the U.S. Census Bureau surveys state and local governments across the country about their revenues and expenditures. This survey makes it possible to compare the finances of state and local government across the 50 states. In PARCA’s analysis of the data, How Alabama Taxes Compare, state and local revenues are considered together because states vary greatly in how they divide up the responsibilities between state and local governments for financing the operation of services like schools, roads, courts, health care, and public safety. In the end, the combined revenue from state and local taxes is used to provide government services. The data for 2016 is the most recent year available.[1] An interactive version of the data is also available through PARCA’s data dashboard.

Rank in Per Capita Tax Collections, 2016

State and Local Tax Sources

Alabama's Rank Among U.S. States

All Taxes

50

Property

50

Individual Income

36

Corporate Income

40

Sales and Gross Receipts

29

General Sales

30

Selective Sales

17

- Alcoholic Beverage

3

- Public Utilities

5

- Motor Fuel

34

- Tobacco Products

35

- Other Selective Sales

32

Motor Vehicle License

45

Other Taxes

25

The most glaring difference between Alabama and other states is our low reliance on property taxes.

Alabama ranks 50th in the U.S. in state and local property tax collections per capita.

If Alabama’s per capita property tax collections matched the average of other Southeastern states:

State and local governments would have an additional $2 billion to spend providing services.

Alabama’s overall tax revenue per capita would rank in the middle of Southeastern states, roughly equaling Mississippi’s tax revenue per capita and putting Alabama above Florida, South Carolina and Tennessee in per capita collections. Alabama would still trail Arkansas, North Carolina, Louisiana, Kentucky, and Georgia.

As it stands, Alabama’s traditional preference for low property taxes leaves state and local governments more reliant on other taxes for revenue. Alabama has among the highest sales tax rates in the U.S. Alabama also has some of the highest taxes per capita on alcohol and public utilities. Despite those higher rates, Alabama doesn’t make up the difference created by its low property tax collections.

Other unusual features of Alabama’s tax system include:

Sales Taxes:

Alabama is one of three states that continue to apply sales tax fully to food purchased for home consumption without providing any offsetting relief for low- and moderate-income families.

Alabama’s sales tax is not as broad as other states and doesn’t apply to most services. Consequently, despite high rates, Alabama’s sales tax isn’t as productive as some other states.

Income Taxes:

Alabama threshold for taxing income is the lowest in the nation. Most states set a higher income threshold than Alabama in order to allow poor households to keep more of the money they earn.

Alabama is one of three states that allows taxpayers to deduct from state income the full amount they pay in federal income taxes. Since federal income tax rates are higher the more you earn, the higher your earnings the larger the deduction for state tax purposes.

As a bottom line, Alabama governments operate with less revenue on a per capita basis than governments in all the other states.

This is not a new finding. This has been true since the early the 1990s. And it underlies the difficulties we face when trying to provide to our citizens the level of government services enjoyed by citizens in other states.

A slight majority of Alabamians oppose building new prisons, but an overwhelming majority support expanding rehabilitation and re-entry programs for people leaving prison, returning nonviolent offenders to the community, and spending more on education.

These are among the key findings of the Public Affairs Research Council of Alabama’s Public Opinion Survey: 2019Edition, released today.

The survey,

conducted in partnership with Samford University and led by Dr. Randolph Horn,

again found high levels of agreement on critical issues facing the state.

Alabamians value

education, rating it a top priority among major

state services. State residents say education investment should be increased, as too little is now spent on education. While not agreeing

on the source of revenue, a majority of residents are willing to pay more in

taxes to increase funding for education.

There is some

evidence that the current tax system is seen

as regressive: majorities of residents say low-income

residents pay too much, and those with higher incomes pay too little.

Consistently high

percentages of Alabamians feel that they

have no say in Montgomery or that state officials do not care what they think suggests that Alabamians do not believe

state government is responsive to their concerns.

Corrections

86% support expanded rehabilitation and re-entry programs for

people in prison.

83% support moving people with nonviolent convictions back to

the community.

58% oppose building new prisons to address overcrowding.

54% believe only violent offenders should go to prison.

Education

74% believe the state spends too little on education.

69% support increasing taxes to support education, but no

single option garners majority support.

Taxes

45% say they pay the right amount of taxes.

45% say lower-income earners pay too much.

52% say upper-income earners pay too little.

Trust in Government

82% support keeping the General Fund and Education Trust Fund

separate.

69% believe state government officials do not care about

their opinions.

57% believe they have no say in state government.

The survey of 410 randomly selected Alabamians was conducted between January 28 and March 3, 2019 and yields a margin of error of +/-4.8 percent.

Jefferson County Mayors Cooperate on Pact to Prevent Intercity Business Poaching

Jefferson County mayors and county commissioners announce a cooperative economic development pact Wednesday at the Jefferson County Courthouse.

Mayors from 22 cities in Jefferson County signed a “Good Neighbor Pledge” Wednesday, committing their cities to a set of economic development ground rules designed to prevent incentive bidding wars and counterproductive poaching between the patchwork of municipalities that comprise the county.

With the Good Neighbor Pledge, the mayors hope to end divisive competition and encourage cooperation in recruiting new business from outside the region. Recruiting businesses from one Jefferson County city to another with incentives costs both cities and results in no net gain for the region.

The Pledge is an outgrowth of the Community Foundation of Greater Birmingham’s efforts to encourage regional cooperation and job growth in Jefferson County, an effort that began by commissioning PARCA to research and report on models of cooperation from across the country. The resulting report, Together We Can, provided information that the Jefferson County Mayors Association built upon to craft the Pledge.

“In the past, our cities tended to compete rather than cooperate,” said Hoover Mayor Frank Brocato. “Today, economic development favors metro areas that work together better as a region.”

The 22 cities represent over 75 percent of the county’s population, including the City of Birmingham, Bessemer, Hoover, Mountain Brook, Vestavia Hills, Homewood, Trussville, Argo, Brighton, Center Point, Clay, Fairfield, Graysville, Lipscomb, Midfield, Mulga, Pleasant Grove, Sylvan Springs, Tarrant, Trafford, Trussville, Vestavia Hills, Warrior, and West Jefferson. The signing of the pledge took place in the Jefferson County Commission chambers and featured Birmingham Mayor Randall Woodfin, Jefferson County Commissioner Steve Ammons, and Jefferson County Mayors Association president, Center Point Mayor Tom Henderson. They were joined by other commissioners and mayors from cities big and small.

The agreement grew out of conversations within the Jefferson County Mayors Association, which were facilitated by the Community Foundation. Of the various cooperative approaches described in Together We Can, the mayors found Denver’s model for encouraging cooperation as the most promising and achievable first step.

In Metro Denver’s effort to unite its sprawling and fragmented region around a unified approach to economic development, one of its first steps was creating a Code of Ethics that spelled out what is acceptable and what isn’t when cities are working to recruit businesses. Denver’s agreement aimed to stop cities from fighting over local business relocation and focus instead on a collective approach to attracting new business from outside the region.

In addition to the Code of Ethics, Denver developed a Metro Mayors Caucus, an issue-oriented regular meeting of area mayors which facilitates communication and cooperation among the region’s cities.

Both ideas helped launch the effort that bore fruit Wednesday. The conversations at the Jefferson County Mayors Association spawned a committee chaired by Mountain Brook Mayor Stewart Welch, which examined Denver’s Code and gathered other examples from across the country including local government agreements in place in Milwaukee, San Diego, Dayton and Cuyahoga County, Ohio; and the Fort Wayne region of Northwest Indiana. The committee then drafted a version for Jefferson County.

Mountain Brook Mayor Stewart Welch prepares to sign the Good Neighbor Pledge.

The Pledge is not a legal document but an agreed upon set of principles and protocols. It establishes an Advisory Consulting Committee to serve as a forum for interpreting the pledge in real-world situations and resolving disputes that might arise.

The mayors pledged not to initiate contact with a business located in another Jefferson County city with the intention of enticing that business to relocate. And if a business is seeking to move from one Jefferson County municipality to another, the mayors pledged not to offer financial incentives to encourage the move.

On the other hand, the Pledge encourages mutual aid in efforts to recruit businesses that are new to Jefferson County.

The Pledge does not apply if a local business is expanding and establishing new operations that will not result in job loss in the original municipality.

Along with the Pledge itself, more comments from the various mayors are available in the news release distributed Wednesday.

Leaders in the Shoals Seek Greater Collaboration

A new report by PARCA, commissioned by the Committee for a Greater Shoals

Energized by a climate of opportunity and a burst of positive attention for the region, civic leaders in the Shoals have launched a new effort to improve the economy and quality of life through cross-community collaboration.

More than 150 people attended the launch of the effort, which is organized by the Committee for a Greater Shoals, a group of Shoals business leaders. The event featured the release of A Greater Shoals: a Pathway, a report authored by PARCA on the current state of the region and avenues of opportunity.

Shortly after the event, 110 people had signed up for one or more of six committees:

Broadening the Definition of Economic Development

Developing High-Tech Infrastructure/Recruiting

Quality of Life

Workforce Development and Education

Unified Tourism

Government Cooperation and Structure.

Off the Interstate corridor and tucked away in the Northwest corner of the state, the Shoals is often described by residents as a well-kept secret. That is part of the region’s charm, but it’s also a frustration.

Taken together, the four cities at the heart of the Shoals — Florence, Muscle Shoals, Sheffield, and Tuscumbia — have a population of over 70,000. A combination of the four adjacent cities would rank as Alabama’s 7th largest city. Leaders in the Shoals have long wondered if the region was held back by the fragmented nature of the Shoals, with four principal cities, and six school systems spread across two counties.

Building off research PARCA performed on the Birmingham metro area, PARCA found evidence that fragmentation did have discernable negative effects in the Shoals but also identified cooperative structures the Shoals has developed to pull the region together.

The report recommended building on those existing cooperative structures to capitalize on immediate opportunities, while embarking on a longer-term process to decrease governmental duplication and work toward greater unity.

The report found success to build on in the area of education. According to PARCA’s analysis, when the K-12 school systems in the Shoals metropolitan area were considered together, they produce a higher college and career readiness rate among high school seniors than any other Alabama area.

The Shoals also has the second highest college-going rate among Alabama MSAs, thanks in part to a local civic initiative, Shoals Scholar Dollars, that provides scholarships for residents of Colbert and Lauderdale counties. The Shoals is home to a community college, Northwest-Shoals Community College, and a four-year university, the University of North Alabama, both of which are poised for growth.

The Shoals has developed vehicles for bringing its counties and cities together in pursuit of economic development, including a unified economic development authority, a unified economic development fund, and a united two-county Chamber of Commerce.

Those cooperative structures create a strong competitive position for the Shoals in pursuing industrial projects, like suppliers for the Toyota-Mazda Manufacturing plant under construction in Huntsville. But they also provide a framework for cooperation on further developing the Shoals natural and cultural assets.

With the Tennessee River running through its heart, the Shoals has unrivaled natural assets, ripe for further recreational development. On the cultural front, the Shoals has enjoyed a surge of national and international attention to the Shoals’ historic and contemporary contributions to American music. That’s drawn a stream of tourists to the FAME and Muscle Shoals Sound Studios. Florence has emerged unexpectedly as a fashion hub, serving as home base for designers Billy Reid and Natalie Chanin. That new interest builds on top of tourist attractions like Helen Keller’s home in Tuscumbia and W.C. Handy’s in Florence. Traditional down towns in Florence, Sheffield, and Tuscumbia have been revitalized with local investment.

A coordinated cooperative effort to build on these strengths would bring more resources and reach, the report observes. Though traditional economic development has focused on developing sites and luring employers with incentives, contemporary economic development includes a focus on developing an ample and high-quality workforce and providing a high quality of life that benefits locals and attracts new residents and businesses.