The thriving economy produced another year of surging tax collections for Alabama’s General Fund and Education Trust Fund (ETF), the two primary accounts that provide state funding for government operations. The better-than-projected results put the state in a good position to meet current obligations and weather a downturn should it arise.

It also appears that budgeting changes made by the Legislature in recent years have created more balance in revenue growth between the two funds.

According to the state’s financial reports for the fiscal year that ended on Sept. 30, the taxes and revenues that feed the General Fund were up 8% over 2018. Revenue to the ETF increased by 7% over the previous year. It is unusual that the General Fund’s rate of growth exceeded the ETF’s. Historically, the ETF, which contains major growth taxes like the income and sales taxes, grows faster than the General Fund.

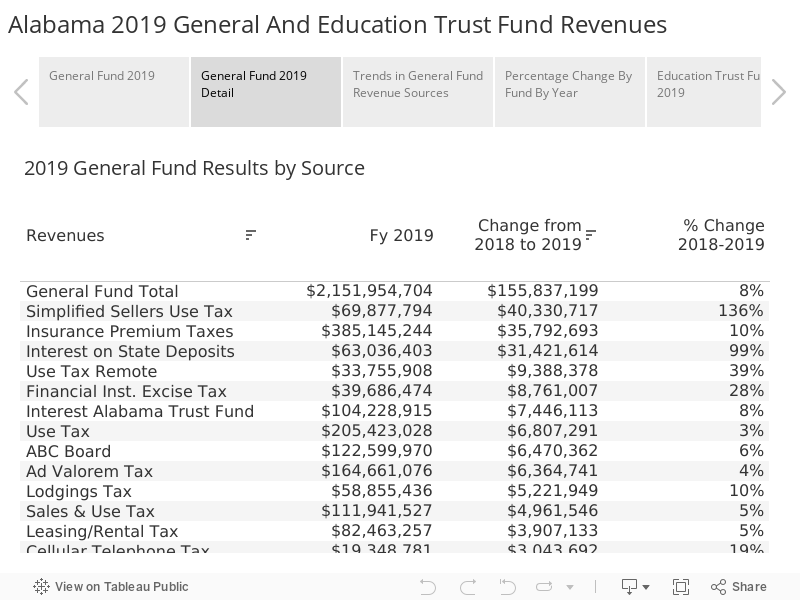

In dollar terms, General Fund revenue increased by $155,837,199.45 to a total of $2,151,954,704, while ETF collections rose by $461,710,824 to $7,215,276,202.89. Collections in both funds exceeded projections.

General Fund

Alabama’s General Fund revenues are derived from a hodgepodge of taxes, most of which moved in a positive direction. General Fund spending supports health programs, like Medicaid and the Departments of Health and Mental Health, as well as law enforcement, the judicial and corrections system and other public safety agencies, plus a variety of other non-education programs.

In dollar terms, revenues from insurance premium taxes are the biggest contributor to the General Fund, providing $385 million or 18% of total collections. Those taxes, which are applied to the premiums paid by insurance policyholders, grew 10 percent over 2018, putting an additional $35 million into the General Fund.

There may be several reasons why this tax is growing at a faster rate than the overall economy. Since more people are employed and have more stable resources, more of them might be buying insurance in contrast to tougher economic times. At the same time, insurance companies may be charging more in premiums as they rebuild reserves needed to cover storm events and rising costs.

The Insurance Premium Tax is set to become an even bigger contributor to the General Fund in future years. A fixed amount of the tax, $31 million, had flowed into the Education Trust Fund. That division of the tax will end, and the total tax will flow into the General Fund. However, the transfer of this revenue comes with the understanding that the General Fund will have to cover the cost of the ALL Kids Children’s Health Insurance Program in future years, an expense that will rise over time.

In percentage terms, the tax that experienced the biggest jump in both its contribution to the General Fund and its rate of increase was the Simplified Sellers Use Tax. This is a tax paid on purchases made over the Internet and delivered to Alabama. Originally established in 2015 as a voluntary method for out-of-state sellers to remit sales tax to the state, the law has been increasingly tightened to require businesses that have significant online sales to participate. A 2018 decision by the U.S. Supreme Court, known as the Wayfair decision, gave further authority to collect taxes on online sales.

As more online retailers came aboard in 2019, General Fund revenue from the source jumped by 136% or $40 million to a total of $70 million for 2019. The General Fund gets 75% of the Simplified Sellers Use Tax. The remaining 25%, amounting to $23 million in 2019, went to the Education Trust Fund. So, the total revenue from the Simplified Sellers Use tax in 2019 rose to $93 million compared to $40 million the year before.

Growth in this tax will likely continue as online sales continue to rise, but the rate of increase should not be nearly as high in the future.

Also helping boost the General Fund were higher interest rates. The interest paid to the state on its cash deposits jumped by $31 million in 2019 to a total of $63 million. Interest rates have subsequently fallen so this revenue source may not be as robust in 2020.

The Use Tax, the General Fund’s second-largest source of revenue, saw a respectable 3% growth, bringing in an additional $6.8 million for a total of $205 million. The Use Tax is collected on out-of-state purchases or leasing of equipment or machinery.

Revenues contributed by the state-regulated alcohol sales were up by 6.5% to $123 million. Property taxes were up 4% to $165 million. The lodging tax jumped 10% to $59 million. Analysts believe a strong year at Baldwin Counties beaches provided a boost, assisted by increased tourism to Montgomery with the opening of the National Peace and Justice Memorial.

Some tax sources declined. Cigarette taxes continued their long slow decline, down 4 percent or $5.6 million. Still, cigarette taxes, which contributed $149 million in 2019, are the 4th largest tax source in the General Fund. Tax collections on vaping products increased 62% but are a very small source of revenue at $2.3 million for the General Fund in 2019.

While the $19 million contributed by the Cellular Phone tax appears to be an increase, base collections actually declined in 2019. The total collections for 2018 were depressed by a refund of the tax paid out as a result of a lawsuit. For the most part, mobile telephone companies no longer charge customers for calls but instead charge for data. Calling plans are taxed; data plans are not subject to tax.

Taxes on automobile titles dropped 6% after several years of gains. The decline could indicate a slowdown in auto sales, a development that would introduce a dark cloud to Alabama’s otherwise sunny economic horizon.

In the interactive chart below, you can compare trends in taxes since 2015. The menu on the right of the chart allows you to decide which taxes appear in the view.

Education Trust Fund

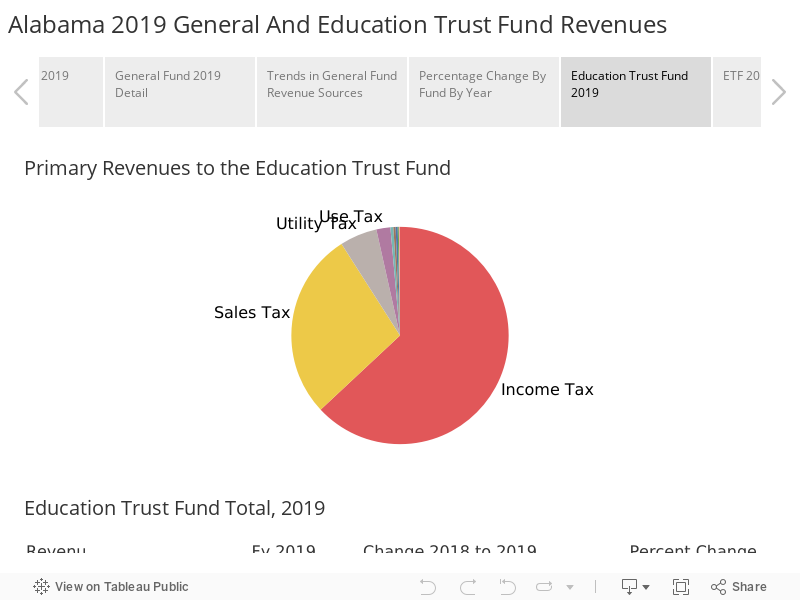

Strong growth in income and solid sales tax growth powered another year of growth in the Education Trust Fund. Those two taxes, both of which are earmarked for education, supply over 90 percent of the education budget. In 2019, income tax collections made up 63% of ETF deposits, while sales taxes contributed 28%.

Income taxes were up $340 million, or 8%, for a total of $4.5 billion. According to financial reports, individual income tax receipts were up 6%, while corporate income taxes increased 15% over 2018. When refunds are taken into account, individuals paid $4.2 billion and corporations $455 million in income taxes.

Along with the general economic growth, the sharper rise in corporate tax collections was likely spurred by the cut in federal corporate income taxes, enacted in December of 2017. Federal income taxes are deductible from Alabama income taxes. With corporations paying less in Federal income taxes, that meant corporations kept a greater share of profits, leaving more corporate income for Alabama to tax.

Sales tax collections rose 6%, to $2 billion, contributing an additional $105 million to the ETF. Total sales tax receipts increased 4%, while the amount held back to pay state agencies decreased. The Department of Human Resources received a smaller sales tax refund because DHR is paying out less in SNAP benefits. The Alabama Department of Revenue also decreased the amount it assessed the state for sales tax collection.

Beyond the income and sales taxes, as noted above, the ETF portion of the Simplified Seller’s Use Tax grew by 136%. In the case of the ETF, that provided an additional $13 million for a total contribution of $23 million. The third-largest contributor to the Education Trust Fund is the utility tax, which brought in $401 million, which was a $5 million or 1% increase over 2018.

Implications of Better-than-Expected Growth

According to Finance Director Kelly Butler, the General Fund ended with a $275 million balance that will be available to appropriate in future budgets.

For the ETF, it’s a little more complicated, due to rules set up under the Rolling Reserve Act, a budgetary control measure designed to curb unsustainable spending and to generate a cushion for use during economic downturns.

According to Butler, the ETF generated an “overage” of $579 million in 2019. Of that, $66.5 million, or 1% of direct budgeted spending in the ETF, will be shifted to the ETF’s Budget Stabilization Fund.

The remaining $512 million will be shifted into the Advancement and Technology Fund. That money will be available for appropriation during the next legislative session to K-12 schools and colleges and universities for spending on non-recurring expenses such as deferred maintenance, school security measures, and educational technology or equipment.

The 7% growth rate for the 2019 ETF will be added to the calculation of the Rolling Reserve’s built-in cap on the growth of education spending. That budget cap is calculated by taking the ETF’s growth rate in each year of the past 15 years, dropping the year with the lowest growth rate, and then finding the average rate of growth for the remaining 14 years.

Despite the good results this year, that overall average will be down slightly. Thus, the allowed rate of growth in spending will be slightly lower in the 2021 budget than it was in the 2020 budget.

That’s because the year dropped from the 15-year window, 2004, was one of the extremely high growth years that preceded the Great Recession. In those years, recurring revenues to the ETF were increasing around 10 percent per year.

The average growth rate will be declining for the next couple of years as those high-growth years drop out of the calculations.

While a final calculation hasn’t been made, it is expected that the spending cap on the 2021 Education Trust Fund Budget will be somewhere between $300 and $400 million over the 2020 Education budget, which totaled $7.1 billion.

It’s important to remember that the Rolling Reserve Act creates a cap on increased spending. The Legislature is in no way obligated to spend up to the cap.

The Bigger Picture

Both the $2 billion General Fund and $7 billion Education Trust Fund are only part of the picture when it comes to paying for the operation of state government agencies. Beyond the tax sources detailed above, other state taxes are earmarked for certain purposes and sent directly to a designated agency.

There are also huge inflows from the federal government, particularly supporting Medicaid and other health programs, road construction and maintenance, and education. The federal contribution is a similar amount to what is generated by state taxes.

Other state agencies generate revenue. Colleges and universities charge tuition. Hunters and fishermen buy licenses that help fund the Department of Conservation and Natural Resources. Companies buy permits that help pay for inspections by the Alabama Department of Environmental Management. Those federal and state revenues are then spent supporting the agencies.

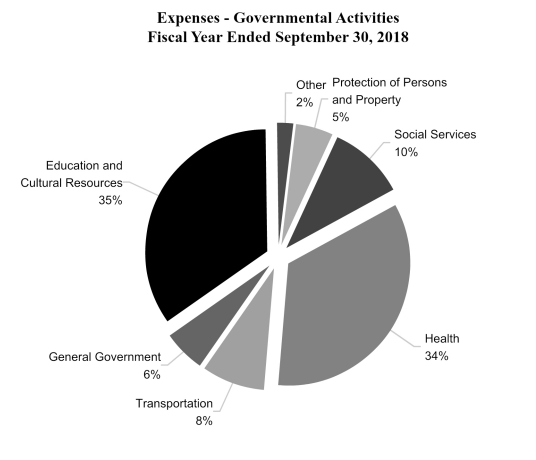

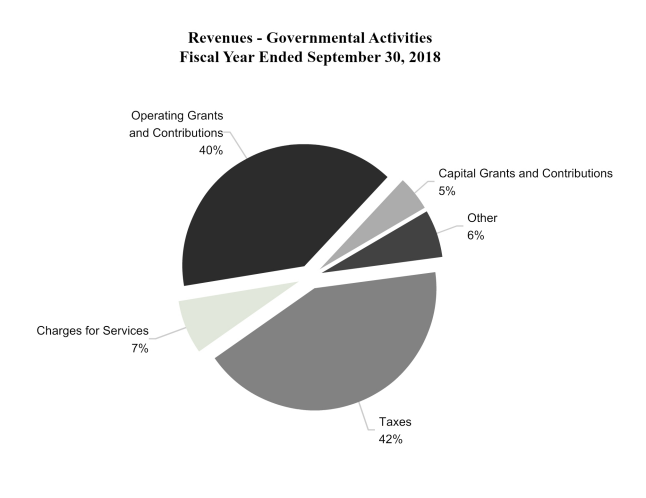

Alabama’s most recent Comprehensive Annual Financial Report (CAFR) details revenues and expenditures for Fiscal Year 2018. In terms of revenue, the CAFR indicates that total revenue was a little over $22 billion, more than double the tax collections deposited into the ETF and General Fund. The CAFR provides the chart below to illustrate the sources and proportion of all the revenues supporting the state governmental activities.

The CAFR also presents the government’s expenses for 2018, broken down by category of spending. On the surface, comparing the sizes of the General Fund and the ETF, it appears that we spend significantly more on education than we do on other functions of government. However, when federal funds and other earmarked taxes and revenues are taken into account, there is a more equal distribution of spending, with about one third spent on education and culture, about one-third spent on health, and one third spent on other functions: roads, law enforcement, the courts, prison, general government.